If you believe your divorce decree automatically removes your ex-spouse from your life insurance and retirement accounts, you're relying on a dangerously fragile safety net. While laws in states like North Carolina, Maryland, and Tennessee offer some protections for your will, they often leave non-probate assets and certain powers of attorney completely exposed. You may feel a sense of relief now that your marriage has ended, yet your former partner could still hold the legal authority to make your medical decisions or inherit your hard-earned legacy. Knowing exactly when to update an estate plan after divorce is the only way to ensure your legal and financial independence is truly permanent.

We understand that after a difficult transition, the last thing you want is more paperwork. It's natural to feel protective of your new future and anxious about ensuring your children are the ones who benefit from your estate. This guide will show you how to systematically revise your legal documents to reclaim total control. We'll explore the specific gaps in state laws and provide a clear path toward the peace of mind that comes from a secure, updated legacy.

Key Takeaways

- Recognize why the period between physical separation and a final decree is the most dangerous time for your assets and medical autonomy.

- Learn why state laws in NC, SC, MD, and TN are insufficient for protecting non-probate assets like 401(k)s and life insurance policies.

- Discover how a Revocable Living Trust provides a layer of privacy and protection that a simple will cannot offer during a major life transition.

- Identify exactly when to update an estate plan after divorce to ensure your ex-spouse cannot control the inheritance you leave for your children.

- Explore how to integrate Medicaid Crisis Planning into your new strategy to preserve your legacy for the next chapter of your life.

The Timeline of Change: When Exactly Should You Update Your Plan?

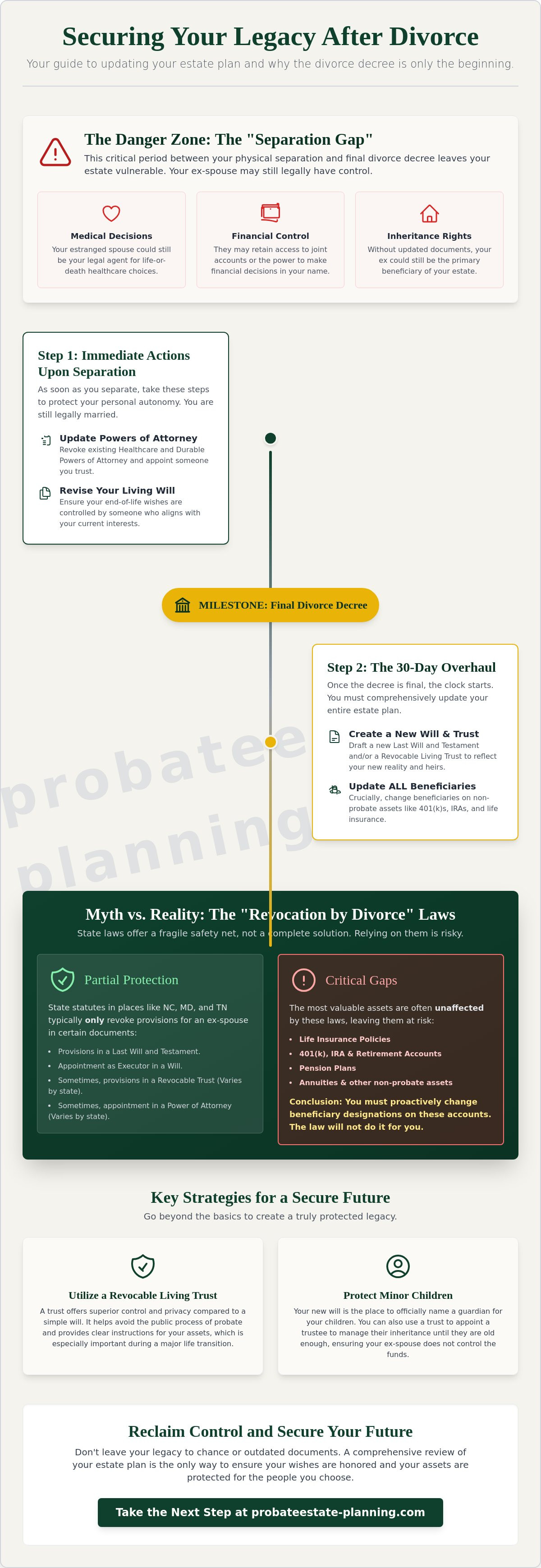

Many people assume they should wait for a final court order before touching their legal documents. This is a dangerous misconception. The "Separation Gap" represents the time between your physical separation and the formal end of your marriage. During this window, you are technically still married in the eyes of the law. If something happens to you now, your estranged spouse likely still holds the keys to your medical care and your finances. Understanding exactly when to update an estate plan after divorce begins long before the final gavel falls.

To protect your autonomy, you must understand the foundational elements of what is an estate plan and how it functions as a living set of instructions. While you can't always disinherit a spouse entirely while still legally married due to "elective share" laws, you can immediately limit their control over your life. These laws generally guarantee a surviving spouse a percentage of the estate, but they don't grant them the right to make your healthcare or daily financial choices. Waiting for a final decree can leave your future in the hands of someone who no longer shares your interests.

To better understand the steps involved in this transition, watch this helpful video:

Updating During the Separation Period

The moment you file for divorce, your priorities shift toward protection. Your first step should be reviewing your Healthcare Power of Attorney and Living Will. Without an update, the person you are currently litigating against remains your legal surrogate for life-support decisions. Similarly, you should update your Durable Power of Attorney. This prevents an estranged partner from accessing your individual bank accounts or making binding financial commitments in your name while your case is pending. These updates provide a vital layer of security during a period of high emotional and financial volatility.

The 30-Day Post-Decree Checklist

Once the judge signs your final decree, the clock starts on a total plan overhaul. This document is the legal trigger that allows you to finalize your new independence. You have about 30 days to ensure your new Last Will and Testament and Revocable Living Trust align perfectly with the terms of your divorce settlement. It's vital to coordinate these documents with any life insurance requirements or property transfers mandated by the court. You must also notify your banks and insurance companies of the change. Relying on "automatic" state revocations is risky because they often fail to cover non-probate assets like 401(k) accounts or private pension plans. Knowing when to update an estate plan after divorce means acting decisively the moment that decree is in your hand to prevent your legacy from falling into the wrong hands.

Revocation by Divorce: Myth vs. Reality in NC, SC, MD, and TN

Many people believe that a final divorce decree acts as a universal "reset" button for their legal affairs. This is a dangerous misconception. While most states have "revocation by divorce" statutes, these laws are often narrow and inconsistent. They act as a fragile safety net rather than a comprehensive shield. Relying on these default fallbacks often leads to unintended consequences where an ex-spouse retains control over vital decisions. If you want to ensure your legacy remains within your control, understanding the necessity of revising your core documents is essential to avoid leaving your future to chance.

State-Specific Statutes You Need to Know

North Carolina General Statute § 31-5.4 automatically revokes all provisions in a will that favor an ex-spouse, including their appointment as an executor. However, it doesn't touch non-probate assets. Maryland law is broader. It revokes provisions in wills and revocable trusts, and it even removes a former spouse as an agent under a power of attorney. Tennessee law provides a different mix; it revokes will provisions and healthcare powers of attorney, but it leaves financial powers of attorney untouched. South Carolina law attempts to cover both probate and non-probate assets, yet it still faces significant hurdles from federal regulations that can override state intent.

The Limits of Automatic Revocation

The biggest danger lies in what these statutes ignore. Retirement accounts like 401(k)s and IRAs are typically governed by ERISA, a federal law. ERISA often ignores state revocation rules entirely. If your ex-spouse is still the named beneficiary on your 401(k), the plan administrator will likely pay them regardless of what your state's divorce laws say. Stale beneficiary designations on life insurance policies present a similar risk. Additionally, property held in joint tenancy with right of survivorship might not automatically convert to a tenancy in common. This means your ex could still inherit the entire property if you pass away before the deed is corrected.

The "Remarriage Trap" adds another layer of complexity. If you remarry without updating your old plan, you create a legal battleground between your new spouse and your former one. This uncertainty causes unnecessary pain for your loved ones during an already difficult time. Proactively managing these details with a professional estate planning review ensures your documents reflect your current reality. Knowing when to update an estate plan after divorce is about more than just legal compliance. It's about protecting the people you love most from avoidable conflict and ensuring your hard-earned assets reach the right hands.

Revising Your Core Documents: Wills, Trusts, and Beneficiaries

Securing your future starts with a clean slate. After a divorce, your previous legal documents likely reflect a life that no longer exists. Since 56% of U.S. adults currently lack any estate planning documents, your divorce is actually a strategic opportunity to build a more robust, protective foundation than you had before. Knowing when to update an estate plan after divorceis just the first step; the real work lies in ensuring your new Last Will and Testament accounts for your current financial reality and your specific wishes for your children. You aren't just removing a name; you're redefining your legacy.

A revocable living trust offers a level of privacy that a simple will cannot provide. Because these trusts avoid the public probate process, the details of your assets and who inherits them remain confidential. This is particularly valuable after a divorce when you may want to keep your newfound financial independence out of the public record. If you have an Irrevocable Trust created during your marriage, the situation is more complex. These documents are designed to be permanent, but we can often explore decanting options or court-ordered modifications to ensure the trust still serves your goals without benefiting a former partner.

Restructuring Your Trust for New Goals

Your trust needs a new captain. It's vital to remove your ex-spouse as a Trustee or Successor Trustee to prevent them from having any authority over your assets. You should also consider adding spendthrift provisions. These clauses protect the inheritance you leave for your children from their own future creditors or potential divorce settlements, ensuring your wealth stays within your family line. Finally, verify that your trust funding is updated. Any assets retitled during your divorce settlement must be properly moved into the trust to avoid unnecessary probate complications later.

Beneficiary Designations and the ERISA Exception

State laws often stop at the probate court's door. As we discussed earlier, federal ERISA rules mean your 401(k) or pension plan might still name your ex-spouse as the primary beneficiary regardless of your divorce decree. You must manually update these designations on every account, including IRAs and life insurance policies. Don't forget to name contingent beneficiaries. This creates a vital backup plan if your primary choice passes away before you. In many cases, naming your revocable living trust as the primary beneficiary simplifies the process. It allows you to control the distribution through one central document rather than managing dozens of individual account forms.

While you're organizing these core documents, it's the ideal time to look ahead at your long-term care needs. A well-structured plan acts as the foundation for future Medicaid Crisis Planning. By organizing your assets now, you're better positioned to protect your remaining estate from being exhausted by nursing home costs later in life. Knowing exactly when to update an estate plan after divorce ensures that every piece of your financial life is working toward your new, independent goals.

Protecting Minor Children and Guardianship Choices

For many parents, the most unsettling realization after a split is that their former partner might still have legal control over their children's financial future. While you likely trust your ex-spouse to care for your children, you may have different philosophies regarding long-term financial management or inheritance. If you pass away without a specific plan, the court often appoints the surviving parent as the guardian of the child's property. This means your ex-spouse could decide how your life insurance proceeds or retirement savings are spent. Determining exactly when to update an estate plan after divorce is vital to preventing this scenario and ensuring your assets are used exactly as you intended.

One of the most effective tools for this transition is a Minor's Trust, often established within your Last Will and Testament or a Revocable Living Trust. This structure allows you to name a specific individual to oversee the funds until your children reach a certain age, such as 25 or 30. It provides a methodical way to provide for their education and health without handing over a large sum of money to a teenager or leaving it to the discretion of an ex-spouse. You should also consider how Social Security Survivor Benefits will support them. These benefits are paid to minor children if a parent passes away; coordinating these payments with your private estate ensures a seamless financial transition for their caregivers.

Naming a Guardian vs. a Financial Trustee

It's a common mistake to assume the person raising your children must also manage their money. These are two distinct roles. You can name a trusted family member as the guardian for daily care while appointing a neutral professional or a different relative as the Successor Trustee for the finances. This separation of powers creates a system of checks and balances that prioritizes the children's best interests. To guide these individuals, we recommend drafting a "Letter of Intent." This non-binding document shares your personal wishes for your children's upbringing, from their religious education to your hopes for their college years, providing a sense of continuity during a difficult time.

Special Considerations for Adult Children and Grandchildren

If your children are already adults, your focus shifts toward protecting them from family conflict. Estate disputes can be emotionally devastating for adult children caught between two parents. Updating your plan allows you to clarify your intentions and use "Per Stirpes" designations. This ensures that if one of your children passes away before you, their share goes directly to your grandchildren rather than being redistributed in a way that might cause resentment. If you've already started educational funds for grandchildren, verify that the successor owners on those accounts are updated. Taking these steps provides the peace of mind that your legacy will support the next generation without interference. If you're ready to secure your children's future, our team can help you update your estate planning documents to reflect your new family structure.

Securing Your Legacy with The Probate & Estate Planning Co.

The transition into a new chapter of life requires more than just a signature on a divorce decree; it demands a strategic reconstruction of your legal safeguards. Our practice provides a steady hand for clients across North Carolina, South Carolina, Maryland, and Tennessee, ensuring that the nuances of each state's statutes don't leave your future exposed. We move beyond the cold technicalities of law to provide a human-centric partnership. Our goal is to transform a daunting professional landscape into a navigable path toward security. Understanding when to update an estate plan after divorce is the first step toward reclaiming your narrative and protecting the interpersonal connections that matter most to you.

A professional audit of your existing documents is the only way to identify hidden vulnerabilities. Many clients are surprised to find that old powers of attorney or outdated trust provisions still grant significant authority to a former spouse. We provide a methodical review of your entire portfolio, ensuring every document reflects your current wishes and your new financial reality. This thoroughness is the signature of our brand, focusing on functional reliability and practical outcomes rather than mere administrative preparation.

Medicaid and Asset Protection After Divorce

Divorce fundamentally changes your long-term care strategy. As a single individual, your Medicaid eligibility and asset spend-down requirements are different than they were during your marriage. Without a spouse to protect "exempt" assets like your home, you face a higher risk of losing your estate to nursing home costs. We integrate Medicaid Crisis Planning into your post-divorce strategy to mitigate these risks. By utilizing tools like an Irrevocable Trust, we can help shield your savings and your home from being exhausted by future medical needs. We ensure your new plan doesn't accidentally disqualify you from benefits, providing a layer of safety that preserves your legacy for your children.

Next Steps: Your Private Consultation

Your first meeting with an estate planning attorney is a private consultation designed specifically for your unique circumstances. To make this session most productive, you should bring your final divorce decree, your current financial statements, and any existing estate documents. We often coordinate directly with your divorce counsel to ensure that property transfers or life insurance requirements mandated by the court are seamlessly integrated into your new estate plan. This collaborative approach ensures no detail is missed and no asset is left unprotected.

Regaining control over your future is a powerful act of responsibility. While the divorce process focuses on the end of a relationship, our work focuses on the beginning of your new independence. We're here to provide the wisdom and experience needed to steer you toward a predictable, secure outcome. When you know exactly when to update an estate plan after divorce and take decisive action, you can move forward with the quiet confidence that your legacy is safe and your future is entirely your own.

Take Command of Your New Beginning

Your divorce marks a significant transition toward independence. You've learned that relying on automatic state revocations is a gamble you don't have to take. From securing non-probate assets to ensuring your children's inheritance is managed by a trusted trustee, the proactive steps you take now define your financial future. Knowing exactly when to update an estate plan after divorce is the key to preventing an ex-spouse from making your medical decisions or unintentionally inheriting your hard-earned assets.

Our team brings specialized expertise in probate and Medicaid Crisis Planning across North Carolina, South Carolina, Maryland, and Tennessee. We offer human-centric guidance to help you navigate these sensitive legal shifts with confidence. We provide more than just documents; we provide a partnership in long-term security. Schedule a consultation to protect your legacy and secure your future. You've successfully navigated the complexities of a major life change. Now it's time to enjoy the quiet confidence that comes with a truly secure and predictable legacy.

Frequently Asked Questions

Does a divorce decree automatically change my life insurance beneficiary?

No, a divorce decree does not automatically change your life insurance beneficiary in most states. While laws in some jurisdictions revoke will provisions, they often don't reach non-probate assets. You must contact your insurance provider directly to submit a new beneficiary designation form. Failing to do this can result in your ex-spouse receiving the payout regardless of your divorce settlement or your current wishes for your children's future.

Can I change my estate plan while my divorce is still pending?

You can and should update parts of your plan while a divorce is pending. While you might be restricted from moving joint assets due to temporary court orders, you can immediately update your Healthcare Power of Attorney and your Last Will and Testament. This ensures that if something happens during the litigation process, your estranged spouse doesn't have the final word on your medical care or your personal estate.

What happens if I die before my divorce is finalized?

If you pass away before the final decree, the law treats you as a married person. Your spouse will likely inherit your assets through your existing will or state intestacy laws. They may also be entitled to an "elective share" of your estate regardless of your wishes. This highlights exactly when to update an estate plan after divorce; starting the process during the separation period provides a vital layer of protection before the marriage officially ends.

Should I remove my ex-spouse from my Healthcare Power of Attorney immediately?

Removing an ex-spouse from your Healthcare Power of Attorney should be a top priority. If you are incapacitated, the person named in this document makes all medical decisions, including life-support choices. Most people prefer to name a sibling, parent, or trusted friend during the separation period to ensure their medical care aligns with their current personal values rather than the interests of an estranged partner.

Do I need a new Will if I move to a different state after my divorce?

Moving to a new state after your divorce is a major life event that requires a legal review. Each state has unique rules regarding probate administration and how they treat "revocation by divorce" for trusts and non-probate assets. A document that was valid in Maryland might face procedural obstacles in South Carolina. Updating your plan ensures it meets local requirements and remains fully enforceable in your new home.

How does divorce affect my Medicaid eligibility in Maryland or North Carolina?

Divorce significantly impacts Medicaid eligibility because you are now viewed as an individual rather than part of a couple. In states like Maryland and North Carolina, you no longer have a "community spouse" who can keep certain assets while you qualify for care. This change makes Medicaid Crisis Planning critical to protect your home and savings from being entirely consumed by long-term care costs as you age.

Can my ex-spouse contest my new Will after our divorce is final?

An ex-spouse can attempt to contest a new Will, but they face a high legal hurdle. Once a divorce is final, they are no longer a legal heir. To succeed, they would typically have to prove you were under undue influence or lacked the mental capacity to sign the document. Keeping your plan updated and professionally drafted is the best way to discourage these types of legacy disputes and protect your heirs.

What is a Successor Trustee and why do I need to rename one after divorce?

A Successor Trustee is the person who manages your Revocable Living Trust if you can't do it yourself. During marriage, most couples name each other in this role. After a split, you need to rename this position to a neutral party or a professional. This ensures your assets are managed for your benefit or the benefit of your children without the control of your former spouse. Knowing when to update an estate plan after divorce includes these vital fiduciary changes.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment