Did you know that in states like North Carolina and Maryland, your entire estate inventory often becomes a matter of public record within 90 days of your passing? It's a sobering thought that your private financial legacy could be viewed by anyone with a computer. You've spent years building your life's work, and it's natural to feel anxiety about that legacy being exposed to public scrutiny or stalled by court delays. Implementing a revocable living trust is the most effective way to shield your family's future from this unnecessary chaos and public exposure.

This guide will show you how this legal tool serves as a private, protective roadmap for your loved ones, allowing you to bypass the public probate process entirely. We'll clarify complex terminology and provide a clear strategy to ensure your assets are managed with care if you ever face a serious illness. You'll learn exactly how this strategy preserves family harmony and provides a seamless transition for your heirs in NC, SC, MD, and TN, giving you the peace of mind that your plan will work when it's needed most.

Key Takeaways

- Discover how to bypass the public, often expensive probate courts in the Southeast and Mid-Atlantic to keep your family's private business out of the public record.

- Understand how a revocable living trust serves as a flexible blueprint for stewardship, allowing you to maintain full control of your assets while ensuring they are protected for the future.

- Learn the essential steps to properly "fund" your trust, moving beyond simple paperwork to ensure your real estate and assets are actually shielded.

- Explore how to safeguard yourself during your lifetime by establishing a plan for incapacity that avoids the stress and cost of court-ordered guardianship.

- Gain clarity on the practical differences between wills and trusts to choose the path that best preserves your legacy and simplifies life for your survivors.

Understanding the Revocable Living Trust: Your Blueprint for Stewardship

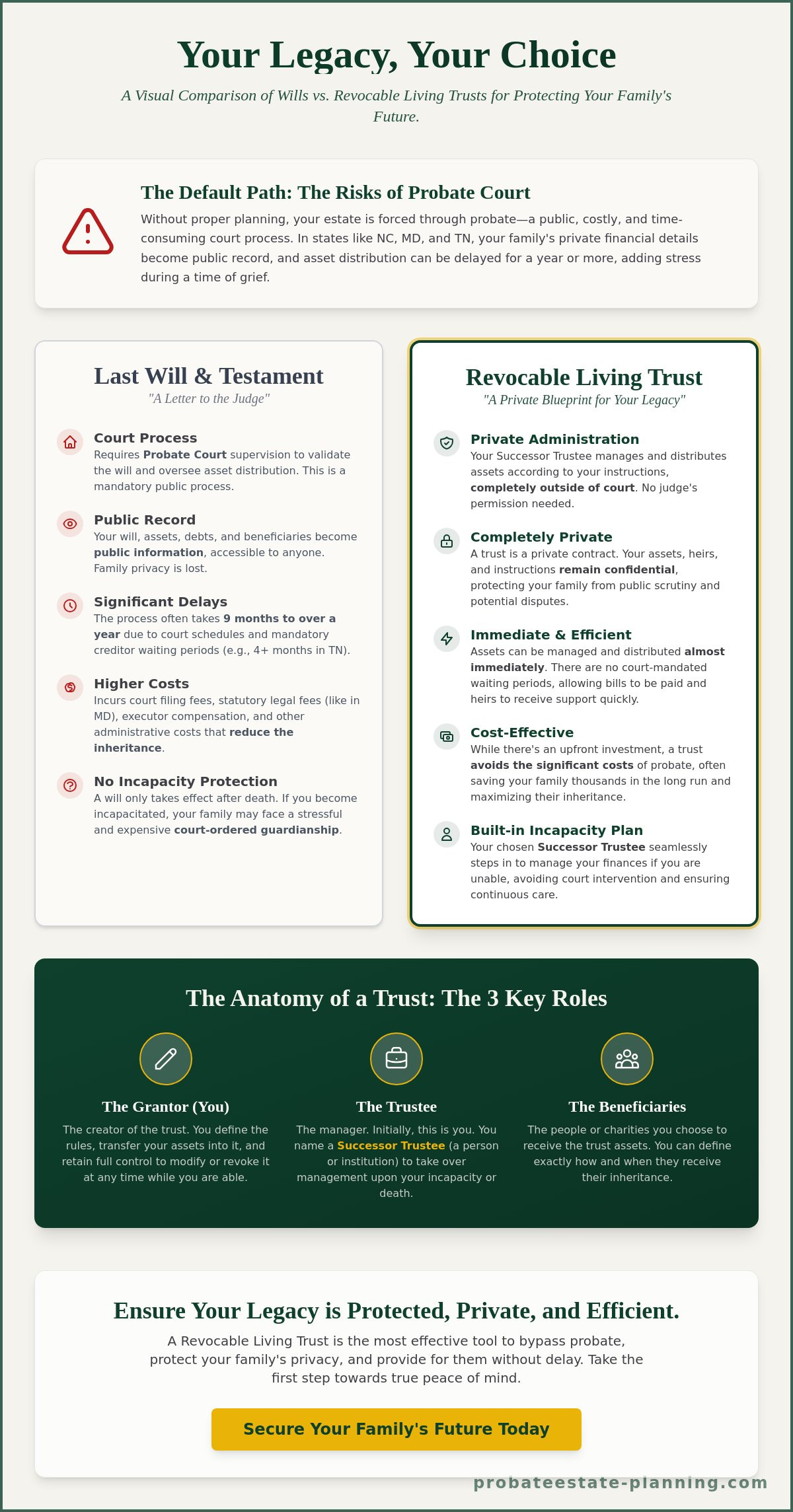

A revocable living trust is more than just a stack of legal papers; it's a flexible "bucket" designed to hold your assets for your benefit while you're alive. This specific legal relationshipallows you to move property into the trust's name without losing an ounce of control over your daily life. You still live in your home, spend your money, and manage your investments exactly as you did before. The primary difference lies in how the law views the "title" of these assets. By shifting ownership from your individual name to the trust, you're practicing stewardship rather than just possession. This distinction is what allows your estate to bypass the public, often stressful process of probate later on.

The "revocable" factor provides the peace of mind you need to plan for the future without feeling trapped. It means you retain the absolute power to change the terms, add or remove assets, or even cancel the trust entirely at any time. Whether you live in North Carolina, South Carolina, Maryland, or Tennessee, this flexibility ensures your plan evolves alongside your family's needs. It isn't a rigid cage; it's a living document that adapts to your life's changing seasons.

The Anatomy of a Trust: Grantor, Trustee, and Beneficiary

To understand how a trust functions, you must recognize the three essential roles that make it work. You begin as the Grantor, the creator and initial decision-maker who defines the legacy. In most cases, you also serve as the initial Trustee. This role carries a fiduciary duty, which is a high legal standard requiring the manager to handle assets with the utmost care and loyalty. Finally, the Beneficiaries are the individuals or charities you've chosen as the ultimate recipients of your life's work. By clearly defining these roles, you create a structured environment where your intentions are protected from ambiguity and external interference.

Successor Trustees: Ensuring a Steady Guide is in Place

Choosing a successor trustee is a critical step in preventing family chaos during a time of grief. This person or entity steps in only when you're no longer able to manage the trust yourself. You might choose an adult child who understands your values, or you may opt for a professional fiduciary, such as a bank or trust company, to ensure objective and expert management. A professional fiduciary often helps maintain family harmony by removing the emotional burden from grieving relatives. The Successor Trustee is the backup pilot for your financial life. Having this person vetted and named in your revocable living trust ensures that your family's protection remains uninterrupted, even in your absence.

Why Families in the Southeast and Mid-Atlantic Choose Trusts Over Wills

Many families across the Southeast and Mid-Atlantic assume a will is the final word in estate planning. While a will is a foundational document, it's essentially a letter of instruction to a probate judge. It doesn't take effect until you pass away, and even then, it requires a court's permission to move assets. A revocable living trust functions as a private, efficient vehicle that keeps your family out of the courtroom entirely. It offers a level of stewardship that a simple will cannot match, ensuring your legacy moves forward without public interference.

The Hidden Costs and Delays of Probate Court

Probate is the court-supervised process of authenticating a will and distributing assets. In states like Maryland and Tennessee, this process is rarely quick. Maryland probate fees follow a statutory schedule that can drain thousands of dollars from an estate before a single heir receives a dime. In Tennessee, state law requires a minimum four-month period for creditors to file claims, which often stretches the total timeline to a year or longer. This delay creates an emotional burden for grieving families who must wait for court orders just to pay basic utility bills or funeral expenses.

Privacy is another casualty of the probate process. Once a will is filed, it becomes a public record. Anyone can see what you owned, what you owed, and exactly who is receiving your property. Families who value discretion choose a trust because it's a private contract. Because the person who creates the document retains the ability to alter the trust during their lifetime, it provides total flexibility while keeping your financial business behind closed doors. This privacy helps maintain family harmony and protects heirs from unwanted solicitation.

Protecting Your Legacy Across State Lines

It's common for residents in our region to own property in multiple states. You might have a primary residence in Maryland but own a vacation home in South Carolina or a family farm in North Carolina. If you rely solely on a will, your family will likely face "ancillary probate." This means your executor must open separate court cases in every state where you owned real estate. This doubles or triples the legal fees, court costs, and administrative headaches for your loved ones.

A revocable living trust acts as a single, unified bridge for your entire estate, regardless of where your property is located. By titling your various holdings into the name of the trust, you consolidate your legacy into one manageable entity. This prevents the chaos of multi-state litigation and ensures your assets are distributed according to one set of rules. If you're concerned about how your out-of-state property might complicate things for your children, you can explore your estate planning options to create a more streamlined path forward. This proactive approach replaces uncertainty with a clear, methodical plan that works the moment it's needed.

The 'Living' Benefit: Managing Incapacity Without Court Intervention

Most people associate estate planning with what happens after they're gone, but the most immediate value of a revocable living trust often arrives while you're still here. Life is unpredictable. A sudden stroke, a car accident, or a progressive diagnosis like Alzheimer's can leave you unable to manage your own affairs. Without a trust, your family may face a "living probate," a public and often painful court process to gain control of your finances.

In states like North Carolina and Tennessee, this court-supervised process is known as guardianship or conservatorship. It requires a judge to declare you legally incompetent. This isn't just emotionally taxing; it's a matter of public record. Your private financial life becomes an open book for the court to scrutinize. By placing your assets in a trust, you ensure a private transition. Your Successor Trustee takes over management of the trust assets immediately. They don't need a judge's permission to pay your mortgage or fund your medical care.

- Immediate Access: Your bills are paid on time, preventing credit damage or service interruptions.

- Privacy: No public hearings are required to prove you need help.

- Specific Guidance: You define exactly what "incapacity" looks like, such as a certification from two independent physicians.

Trusts vs. Powers of Attorney: A Two-Pronged Defense

You still need a Durable Power of Attorney, but it isn't a replacement for a trust. Financial institutions in Maryland and South Carolina can sometimes be hesitant to honor older Power of Attorney documents, leading to delays when every day matters. A revocable living trust is a robust legal contract that banks generally respect with fewer hurdles. While the Power of Attorney handles things like Social Security or tax filings, the trust serves as a detailed instruction manual for your care. You can specify the quality of life you want and how your resources should be spent to maintain it.

Maintaining Harmony During Difficult Times

A medical crisis is already stressful for your spouse or children. They shouldn't have to guess your wishes or fight over who's in charge. Clear instructions within your trust prevent family friction. When you've clearly outlined that you prefer in-home care over a facility, or specified which assets should be liquidated first to pay for treatment, you're removing a massive emotional weight from your loved ones. This clarity preserves your dignity. It ensures your financial security remains intact during your most vulnerable years, allowing your family to focus on your recovery rather than legal paperwork.

The Path to Protection: How to Properly Fund Your Living Trust

Think of your revocable living trust as a sturdy, handcrafted bucket. While the craftsmanship of the bucket is vital, it cannot provide nourishment if it remains empty. Many families believe the work is finished once they sign their revocable living trust documents. However, a trust without assets is merely a piece of paper that offers no protection against the probate court. To secure your legacy, you must fill the bucket by transferring ownership of your property into the name of the trust.

Re-titling real estate is the first priority. Whether you own a family home in Charlotte, a rental property in Nashville, or a condo in Baltimore, the deed must be updated. This process formally changes the owner from your individual name to the name of your trust. Similarly, your financial accounts require coordination. You don't necessarily need to close your bank accounts; instead, you update the ownership or "payable on death" instructions to align with your new estate plan. The Pour-Over Will acts as your safety net during this transition. If you accidentally leave an asset outside the trust, this document "pours" that asset into the trust upon your death. While this prevents the asset from following state intestacy laws, it usually requires a probate proceeding to function, which is why manual funding is so critical.

Step-by-Step: Moving Assets into Your Trust

Trust Funding is the physical act of transferring title to your legacy vessel. In North and South Carolina, this involves recording new deeds with the County Register of Deeds to reflect the trust as the owner. For life insurance policies and retirement accounts, you must submit specific change-of-beneficiary forms to each carrier. While retirement accounts often stay in your name for tax reasons, your trust can be named as a primary or secondary beneficiary to ensure your wishes are followed without interference.

Common Funding Mistakes to Avoid

Procrastination is the greatest threat to a successful estate plan. According to the 2024 Wills and Estate Planning Study, while 32% of Americans have estate documents, a significant portion fail to complete the funding process. If you don't move your assets, your family must face the exact probate delays you intended to avoid, which often last between 9 and 18 months in many jurisdictions. Failing to fund the trust forces your loved ones back into a public court process, inviting the chaos and expense you worked so hard to prevent. Our firm provides a partnership in stewardship, guiding you through every signature and deed recording to ensure your funding is completed correctly. Contact us today to ensure your assets are protected and your legacy is secure.

Is a Revocable Living Trust Right for Your Family?

Deciding between a traditional will and a revocable living trust is a choice between convenience now or peace of mind later. A will is often less expensive to draft initially, yet it guarantees that your family must enter the public probate system. In states like Maryland and South Carolina, probate can last anywhere from six months to two years. During this time, your assets may be frozen, and your family's private financial details become a matter of public record. This creates an unnecessary burden during a time of grief.

The idea that trusts are only for the ultra-wealthy is a common myth. A trust actually simplifies life for your survivors by moving the legal work to the present day. By funding a trust now, you ensure that your assets transfer to your beneficiaries without a court's permission. This prevents the administrative chaos that often follows a death. However, a will might be sufficient if your estate is simple, you don't own real estate, and your total assets fall below state-specific small estate thresholds, such as the $50,000 limit for small estates in Tennessee.

At The Probate & Estate Planning Co., we focus on plans that function when they are needed most. We don't just hand you a stack of papers; we help you build a framework that protects your family from unnecessary legal fees and emotional strain. Our goal is to ensure your instructions are followed exactly as you intended, without the interference of a courtroom.

Making an Informed Decision for Your Legacy

Your planning must account for the shifting legal landscape. On December 31, 2025, many current tax protections are set to sunset, which may expose more families to estate taxes in 2026. A "one-size-fits-all" form from a website cannot account for the specific nuances of North Carolina or Maryland statutes. These generic documents often fail in state-specific courts, leaving families to deal with the very probate mess they tried to avoid. A professional consultation helps identify these hidden risks, ensuring your plan reflects your actual family dynamics and your current asset profile.

Next Steps: Securing Your Family's Future

The best way to begin is with an honest conversation. Tell your loved ones that you are taking steps to ensure their stability. This transparency builds trust and prevents future disputes. You can Explore our Probate Administration Services to see the difficult processes we help families avoid through the use of a revocable living trust. Knowing your legacy is secure provides a level of comfort that no bank account balance can match.

Our team acts as your steady guide, helping you navigate these choices with clarity and confidence. Don't leave your family's harmony to chance. Schedule a consultation with our steady guides today to begin protecting what matters most.

Your Path to Lasting Family Harmony

Choosing a revocable living trust isn't just about signing legal documents. It's a commitment to your family's future stability. By moving assets into a trust, you effectively bypass the public probate process, which frequently lasts 12 months or longer according to average court timelines in states like North Carolina and Maryland. This proactive step ensures that if you're ever unable to make decisions, a trusted successor steps in immediately without the need for a court order. We've spent years guiding families through the specific statutes of NC, SC, MD, and TN to replace potential legal chaos with a clear blueprint for stewardship. Our human-centric approach focuses on your emotional well-being and preserving your interpersonal relationships through every stage of life. You don't have to navigate these complex requirements alone. We bring a proven track record of helping clients avoid the delays and emotional strain associated with traditional estate administration across our four service states. Secure your family's future with a plan that works; contact us for a consultation.

You've worked hard to build your legacy, and we're here to help you protect it with confidence and care.

Frequently Asked Questions

Does a revocable living trust reduce my income taxes in 2026?

A revocable living trust doesn't reduce your personal income taxes in 2026 or any other year because it's a grantor trust for tax purposes. You'll continue to report all income on your personal Form 1040 just as you did before the trust existed. While the Tax Cuts and Jobs Act provisions expire on December 31, 2025, potentially lowering estate tax exemptions to $7 million, your annual income tax obligations remain unchanged by this document.

Can I change my trust after it has been signed and notarized?

You can change or revoke your trust at any time as long as you have the mental capacity to do so. This flexibility is the defining feature of a revocable living trust. You may update your beneficiaries, change your successor trustees, or add new assets by executing a formal amendment or a restatement. Most clients review their plans every 3 to 5 years to ensure the document still reflects their family's current needs.

What happens to my revocable living trust if I move from North Carolina to Maryland?

Your trust remains legally valid when you move from North Carolina to Maryland, but you should have a local attorney review it immediately. Maryland has specific statutes, like the Maryland Trust Act of 2014, that may offer different administrative advantages than North Carolina laws. Updating your governing law ensures your estate avoids the 10 percent to 15 percent administrative delays often caused by out of state document conflicts during the settlement process.

Is my house protected from creditors if I put it in a revocable trust?

Placing your house in a revocable trust doesn't protect it from your personal creditors during your lifetime. Since you retain total control over the assets, courts view the property as yours for debt collection purposes. If a creditor wins a judgment against you, they can still attach a lien to the home. For asset protection, you'd need an irrevocable structure, which requires giving up your right to change the trust's terms.

Do I still need a Will if I have a revocable living trust?

You still need a specific type of Will, known as a Pour-Over Will, to act as a safety net for your estate. This document ensures that any assets you forgot to retitle into the trust during your life are transferred into it upon your death. Without this 4 to 10 page document, those forgotten assets must go through the standard probate process, which can take 9 to 18 months in states like Tennessee or South Carolina.

How much does it cost to maintain a revocable living trust every year?

There are typically no annual fees or separate tax filings required to maintain a revocable living trust while you're alive. You don't need a separate tax identification number; you'll use your Social Security number for all related accounts. Your only ongoing responsibilities involve the time it takes to ensure new assets, like a 401k or a new home, are properly titled in the trust's name to avoid future probate expenses.

Can I name my adult child as both my Successor Trustee and a Beneficiary?

You can absolutely name your adult child to serve as both your Successor Trustee and a Beneficiary. This is a common choice for about 75 percent of families who want a trusted relative to manage the distribution of their legacy. Your child will have a fiduciary duty to follow your instructions exactly as written. This dual role simplifies the transition and helps maintain family harmony by keeping the administration within the household you trust most.

What is the difference between a revocable trust and a living will?

A revocable trust manages your financial assets, while a living will outlines your medical preferences for end of life care. The trust ensures your home and bank accounts are protected and distributed according to your wishes after you pass. In contrast, a living will only takes effect if you're terminally ill or permanently unconscious. Both are essential components of a 5 part comprehensive estate plan, but they serve entirely different protective functions.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment