What if the $19,000 gift you gave your grandchild today becomes the very reason the state denies your healthcare coverage years down the line? For many families, the medicaid look back period south carolina enforces feels like a trap designed to penalize generosity. It's deeply stressful to realize that a simple act of kindness could jeopardize your future security or the inheritance you've spent a lifetime building. You deserve to feel confident that your legacy is protected, even when life takes an unexpected turn.

We understand the weight of these concerns, especially when a sudden health decline makes long-term care an immediate necessity rather than a distant possibility. You shouldn't have to choose between receiving quality care and losing the family home to estate recovery. This guide provides a clear path through the 60-month rule, offering professional insight into how you can safeguard your assets. We'll explore the 2026 income and asset limits, explain how to handle transfers that might trigger a penalty, and show you that it's never too late to find a protective solution for your family's future.

Key Takeaways

- Understand how the 60-month medicaid look back period south carolina uses allows the state to review every financial transaction you've made before you apply for benefits.

- Learn how the state uses a penalty divisor to calculate specific periods of ineligibility, ensuring you can plan for the exact timing of your coverage.

- Identify specific legal exceptions for family members that could allow for the safe transfer of your home while maintaining your eligibility for long-term care.

- Discover why it's never too late to protect your estate, even in a medical crisis, by using strategies to correct previous transfer errors.

- Prepare for a successful application by conducting a thorough review of your financial history to avoid the stress of unexpected delays or denials.

Understanding the 60-Month Medicaid Look-Back Rule in South Carolina

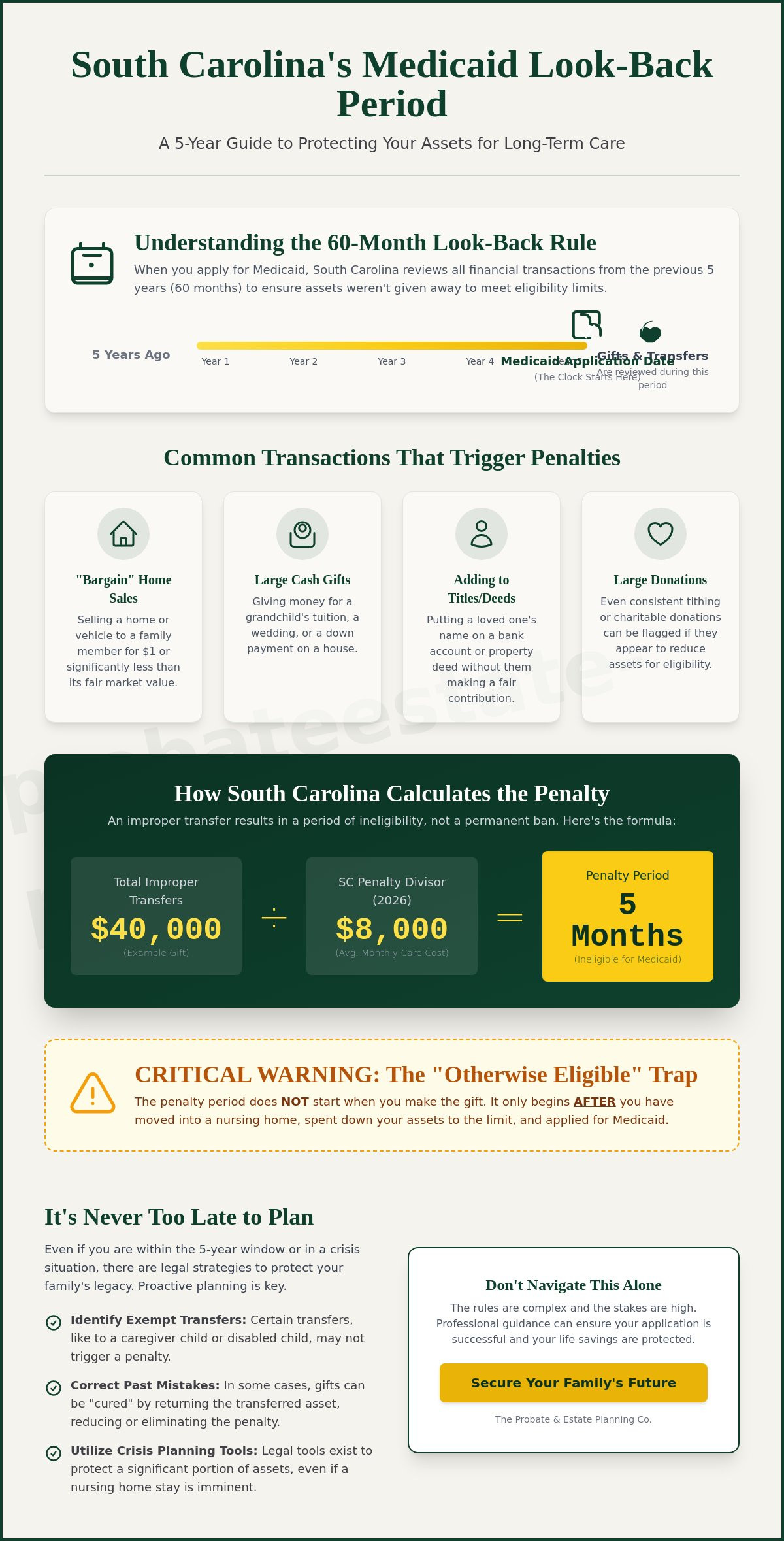

When you apply for long-term care assistance, the state doesn't just look at what you own today. The medicaid look back period south carolina enforces is a strict 60-month investigative window that begins the moment you submit your application. During this time, the South Carolina Department of Health and Human Services (SCDHHS), through its Healthy Connections program, scrutinizes every financial move you've made. They look for any instance where assets were transferred, gifted, or sold for less than what they were actually worth.

The core purpose of this rule is to ensure that the Medicaid program remains a safety net for those who truly lack the resources to pay for nursing home care. By reviewing five years of bank statements, property deeds, and tax returns, the state prevents applicants from giving away their wealth to family members just to meet the $2,000 individual asset limit. While this may feel like an invasion of privacy, understanding this window is the first step toward protecting your family's legacy legally and ethically.

When Does the Clock Actually Start Ticking?

A common point of confusion for many South Carolina residents is when this five-year period begins. The clock doesn't start when you make a gift; it is measured backward from the date of your application. If you gave your daughter a portion of your estate in 2022 and apply for Medicaid in 2026, that gift falls squarely within the look-back window. Proactive planning often involves a strategy of waiting out the clock, where transfers are made early enough that they eventually fall outside the state's reach. SCDHHS is meticulous in its search, using automated systems to track property deed transfers and large withdrawals from financial institutions to ensure no stone is left unturned.

Common Transactions That Trigger SCDHHS Scrutiny

Many people inadvertently trigger a penalty because they don't realize what the state defines as a transfer. It isn't just about large sums of money. SCDHHS looks for any transaction where you did not receive fair market value in return. Some frequent triggers include:

- Family "Bargain" Sales: Selling your home or a vehicle to a child for $1 or any amount significantly below its appraised value.

- Intergenerational Gifts: Providing cash for a grandchild's college tuition, a wedding, or a down payment on a house.

- Titling Changes: Adding a loved one's name to your bank account or property deed without them providing a financial contribution equal to the share they received.

- Charitable Donations: Even consistent tithing or donations to a non-profit can be flagged if they appear to be an attempt to reduce your countable assets.

Each of these actions can lead to a period of ineligibility, but they don't have to be the end of your planning journey. With the right guidance, even recent transfers can often be addressed to minimize their impact on your future care.

Calculating the Penalty: How South Carolina Determines Ineligibility

If you've made a transfer that violates the medicaid look back period south carolina enforces, you aren't permanently banned from receiving help. Instead, the state imposes a "penalty period." This is a specific duration of time during which you are required to pay for your own care out of pocket before Medicaid benefits begin. This rule exists to ensure that individuals don't simply give away their wealth to qualify for public assistance while the state picks up the tab for their long-term care.

South Carolina calculates this period using a "penalty divisor," which represents the average monthly cost of private-pay nursing home care in the state. For 2026, this divisor is approximately $8,000. To find your penalty, the state takes the total value of all improper transfers and divides it by that $8,000 figure. For example, if you gifted $40,000 to your children, you would face a five-month penalty ($40,000 divided by $8,000). During those five months, you'll be responsible for every dollar of your nursing home bills.

The 'Otherwise Eligible' Trap

Many families mistakenly believe the penalty begins on the day they make a gift. This is a dangerous assumption that often leads to financial crisis. In reality, the penalty clock only starts ticking when you have moved into a nursing home, applied for Medicaid, and are "otherwise eligible" for benefits. This means you must have already spent your assets down to the $2,000 limit before the penalty even begins. For an SC applicant, the penalty period start date is the date you would have been eligible for Medicaid benefits if the improper transfer had never occurred. Understanding how the medicaid look back period south carolina uses impacts your timeline is essential for avoiding this trap.

Partial Months and Multiple Transfers

SCDHHS is meticulous with its math and does not round down in your favor. If a gift doesn't divide perfectly into whole months, the state calculates a partial month penalty using a daily rate. With the 2026 monthly divisor at $8,000, the daily penalty is roughly $266.67. Additionally, the state "stacks" multiple transfers. If you gave away $2,000 every Christmas for five years, SCDHHS will add those gifts together into one $10,000 total to determine your full penalty period.

If you're concerned that past generosity might delay your care, exploring asset protection planning can provide a structured way to manage these risks. Engaging in Medicaid crisis planning with a professional ensures you aren't blindsided by these calculations during a sensitive transition, allowing you to maintain control over your financial future.

Exemptions and Safe Transfers: What South Carolina Allows

While the medicaid look back period south carolina enforces is strict, it isn't an absolute barrier to protecting your legacy. The state recognizes that certain transfers are made for legitimate family support rather than simply to qualify for public assistance. Understanding these "safe harbors" can help you preserve your family home and other vital assets without triggering the penalty periods that often catch families off guard. These exceptions are designed to reward family caregiving and protect the most vulnerable members of your household.

One of the most valuable tools is the Caregiver Child Exception. If a child has lived in your primary residence for at least two years immediately before you enter a nursing home, and their care actually delayed your need for institutionalization, you may be able to transfer the home's title to them penalty-free. Similarly, the Sibling Exception allows for a home transfer if your sibling has an equity interest in the property and has lived there for at least one year prior to your application. Transfers made to a spouse or to a child who is blind or permanently disabled are also generally exempt from the 60-month review, providing a vital safety net for those who depend on you.

The Role of the Community Spouse

South Carolina provides specific protections for the "community spouse," which is the partner who remains living at home. Under the 2026 guidelines, the state allows the non-applicant spouse to retain a Community Spouse Resource Allowance (CSRA) of up to $66,480. Shifting assets to a healthy spouse is a protected move that does not trigger look-back penalties. Additionally, the Monthly Maintenance Needs Allowance (MMNA) ensures that the stay-at-home spouse can keep a monthly income of up to $4,066.50. These rules exist to ensure that one partner's need for care doesn't leave the other in a state of financial ruin.

Spending Down Without Penalties

You can also reduce your countable assets by spending funds on "Fair Market Value" (FMV) items or services. This isn't considered gifting because you're receiving something of equal value in return. Safe ways to spend down include paying off an existing mortgage, making necessary home repairs, or purchasing a prepaid funeral contract. You might also choose to buy new medical equipment or modify your home with safety features like ramps and grab bars.

Accuracy is vital during this process. You must keep meticulous receipts for every transaction to prove to SCDHHS that you didn't simply give the money away. Buying a new primary residence or improving your current one is often a wise move because the home is typically an exempt asset during your lifetime. If you're unsure whether a specific purchase might be flagged, consulting an expert in estate planning can help ensure your strategy remains compliant with the medicaid look back period south carolina requires.

Crisis Planning: Asset Protection Within the 5-Year Window

Many families believe they've missed their chance if they haven't planned five years in advance. This is a common misconception that often leads to unnecessary despair. Even if you're already facing the medicaid look back period south carolina enforces, there are still legal pathways to protect a significant portion of your estate. Crisis planning is about reacting to an immediate need for care while using the state's own rules to preserve what you've worked for. It's about finding a steady path forward when things feel most uncertain.

One effective method for correcting past mistakes is the "Gift and Return" strategy. If you realize a recent gift will trigger a penalty, having the recipient return those assets can "cure" the violation. SCDHHS typically treats a full return as if the transfer never occurred, effectively erasing the penalty period. For those with excess cash, a Medicaid Compliant Annuity can transform "countable" assets into a monthly income stream. This removes the lump sum from your asset total while providing funds to help cover costs. Another advanced technique is the "Half-a-Loaf" strategy. This involves gifting roughly half of your remaining assets and using the other half to pay for your care during the resulting penalty period. By the time your retained funds are exhausted, the penalty has expired, and Medicaid coverage can begin.

Strategic Use of Irrevocable Trusts

An Irrevocable Medicaid Asset Protection Trust (MAPT) is a cornerstone of long-term security in South Carolina. When you place assets into this type of trust, you relinquish control to a trustee, which removes those assets from your "countable" estate. It's a trade-off: you lose the ability to manage the assets directly, but you gain the peace of mind that they are shielded from nursing home costs. It's vital to understand that a Revocable Living Trust, while excellent for avoiding probate, offers zero protection against the look-back period. Because you can still access the funds in a revocable trust, the state considers them fully available to pay for your care.

The Importance of Legal Counsel in a Crisis

Attempting DIY Medicaid planning during a health crisis often leads to catastrophic financial loss. The rules are dense, and a single misfiled document or poorly timed gift can result in months of denied coverage. A specialized attorney doesn't just fill out forms; they coordinate directly with SCDHHS to minimize penalty days and ensure every exemption is utilized. This professional partnership turns a daunting legal process into a manageable plan for your family's future. You don't have to navigate these waters alone. Learn more about our Medicaid Crisis Planning services to see how we can help you find stability. If you're currently in the middle of a transition, you should speak with a specialist today to explore your options.

Partnering with The Probate & Estate Planning Co. for Peace of Mind

Facing the medicaid look back period south carolina requires can feel like walking through a minefield where one wrong step threatens your family's financial stability. At The Probate & Estate Planning Co., we believe you shouldn't have to face these complex legal transitions alone. Our team provides more than just administrative filing; we offer an empathetic partnership grounded in professional authority. We understand that behind every bank statement and property deed is a lifetime of hard work and a family's hope for the future. Whether you are in Columbia, Charleston, Greenville, or anywhere else across the state, we are dedicated to safeguarding your legacy with the seriousness it deserves.

We provide a comprehensive review of your financial history to identify risks before they become legal obstacles. Our approach moves away from cold, clinical technicalities toward a protective stance that prioritizes your emotional well-being alongside your formal security. We don't just manage tasks. We safeguard interpersonal connections by ensuring your assets are preserved for the next generation. This clarity empowers you, making the daunting professional landscape feel manageable rather than overwhelming.

Your Steady Guide Through the Medicaid Maze

We act as mentors throughout the entire planning process, guiding you away from confusion toward human-centric solutions. Navigating the SCDHHS application and appeals process is often overwhelming for families already dealing with a health crisis. Our experience allows us to anticipate procedural obstacles before they become costly delays. We focus on functional reliability, ensuring that your asset protection planning actually works when you need it most. By prioritizing your long-term security, we help you maintain the quality of care you deserve without sacrificing the inheritance you've spent years building. We believe in practical outcomes over mere preparation, offering a partnership in long-term management that you can trust.

Take the First Step Toward Security

The most effective way to address your concerns is to identify potential risks as early as possible. A detailed consultation allows us to spot 'red flags' in your 5-year history that might trigger a penalty before you ever submit an application. We offer a methodical, step-by-step solution tailored to your unique circumstances, moving you from a state of anxiety toward a predictable and secure outcome. Our steady pace mirrors the thoroughness required in detailed planning, instilling a sense of trust through our meticulous attention to detail. If you are ready to secure your future and protect your loved ones from future complications, it's time to take action. Schedule your Medicaid planning consultation today to begin building a protective shield around your estate and your family's future.

Taking Control of Your Long-Term Security

Protecting your life's work from the high costs of long-term care is one of the most significant responsibilities you'll face. You've learned that the medicaid look back period south carolinauses is not an impassable wall, but a window that can be managed through legal exceptions and strategic crisis planning. By understanding the 60-month rule and utilizing tools like the caregiver child exception or Medicaid-compliant annuities, you can ensure your family home remains a legacy rather than a source of estate recovery.

Our practice brings specialized expertise in SCDHHS regulations to help you navigate these sensitive transitions with confidence. We provide empathetic, mentor-led guidance designed to alleviate the anxiety of legal uncertainty. As a multi-state practice with a dedicated local focus on South Carolina, we understand the nuances of our state's laws and the importance of preserving your family's future. It's never too late to find a path forward that prioritizes your care and your loved ones' security. Secure your family's future—Schedule a Medicaid Planning Consultation with us today. You deserve the peace of mind that comes with a steady, reliable guide.

Frequently Asked Questions

What is the current Medicaid penalty divisor in South Carolina for 2026?

The 2026 penalty divisor in South Carolina is approximately $8,000 per month. This figure represents the state's average monthly private pay nursing home rate and is updated annually. When you apply for benefits, SCDHHS divides the total value of any improper transfers by this $8,000 amount to determine exactly how many months you will be ineligible for Medicaid coverage.

Can SCDHHS take my home if I am in a nursing home?

The state generally cannot seize your home during your lifetime if you intend to return to it or if a spouse lives there. However, South Carolina's Medicaid program can seek reimbursement from your estate after your death if the home passes through probate. This process, known as estate recovery, makes it essential to use protective legal structures to ensure your home stays in the family.

Does the 5-year look-back apply to my spouse's bank accounts?

Yes, the medicaid look back period south carolina enforces applies to the assets of both spouses, regardless of whose name is on the account. While the non-applicant spouse can keep a Community Spouse Resource Allowance of up to $66,480, any amount over this limit is considered a countable resource. All transfers from either spouse's accounts during the 60-month window are subject to state scrutiny.

What happens if I gave money to my church within the last five years?

Charitable donations and tithing are treated as improper transfers if they occur within the 60-month look-back window. Even if you have a long history of regular giving, the state views these as gifts because you didn't receive fair market value in return. These donations will be totaled and used to calculate a penalty period, which can delay your eligibility for nursing home care.

Can I sell my house to my son for $10 and still qualify for Medicaid?

No, selling your home for $10 will trigger a significant penalty period because it is a transfer for less than fair market value. SCDHHS will determine the actual appraised value of the home and treat the difference as a gift. For example, selling a $200,000 home for $10 would result in a penalty of roughly 25 months based on the 2026 divisor.

Is there any way to shorten the Medicaid penalty period in SC?

The most direct way to shorten a penalty is through a "cure," where the recipient returns the gifted assets to you. If the full value is returned, SCDHHS treats the situation as if the transfer never occurred. Other crisis planning strategies, such as using a Medicaid-compliant annuity, can help provide the income needed to pay for care while you wait for a penalty period to expire.

What is the difference between 'exempt' and 'non-countable' assets in South Carolina?

Exempt assets, such as your primary home or one vehicle, are not counted toward the $2,000 individual limit but may be subject to estate recovery later. Non-countable assets are resources the state ignores entirely during the application process. Understanding this distinction is vital because while an asset might not prevent you from qualifying today, it could still be at risk of being seized after you pass away.

How do I prove a transfer was not made specifically to qualify for Medicaid?

You must provide clear and convincing evidence that the gift was made exclusively for a purpose other than qualifying for benefits. This is a difficult standard to meet and usually requires documentation of your health and financial status at the time of the gift. If you were healthy and had no reason to expect a need for long-term care when the transfer occurred, the state might waive the penalty.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment