Imagine spending forty years building a life in Tennessee, only to see your entire legacy vanish in less than two years because of a single health crisis. With the average nursing home in Tennessee now costing approximately $7,200 every single month, it's understandable why so many families feel a sense of dread. You've worked hard for your home and your savings, and the fear of the 5-year look-back rule shouldn't keep you up at night. Learning how to protect assets from nursing home in tennessee is not about hiding money; it's about the responsible stewardship of your family's future and your own peace of mind.

You're likely looking for a way to ensure your spouse stays comfortable and your children receive their inheritance. You deserve a plan that actually works when it's needed most. In this 2026 guide, you'll discover the legal strategies and TennCare rules designed to safeguard your property and nest egg from being exhausted by long-term care costs. We'll provide a clear, methodical look at how to qualify for benefits while keeping your family home in the family and protecting the assets your healthy spouse needs to live securely.

Key Takeaways

- Learn how the 60-month look-back period impacts your eligibility and why simple gifting can inadvertently trigger harsh financial penalties.

- Explore why Medicaid Asset Protection Trusts are the preferred strategy for Tennessee families seeking to shield their property from state recovery.

- Discover "Half-a-Loaf" strategies that allow you to preserve significant assets even if a loved one requires immediate nursing home placement.

- Understand specific TennCare exemptions and legal instruments that show you how to protect assets from nursing home in tennessee while keeping the family home secure.

- Identify the critical differences between mere document preparation and a comprehensive plan that ensures long-term family harmony and financial stewardship.

The Financial Threat of Long-Term Care in Tennessee

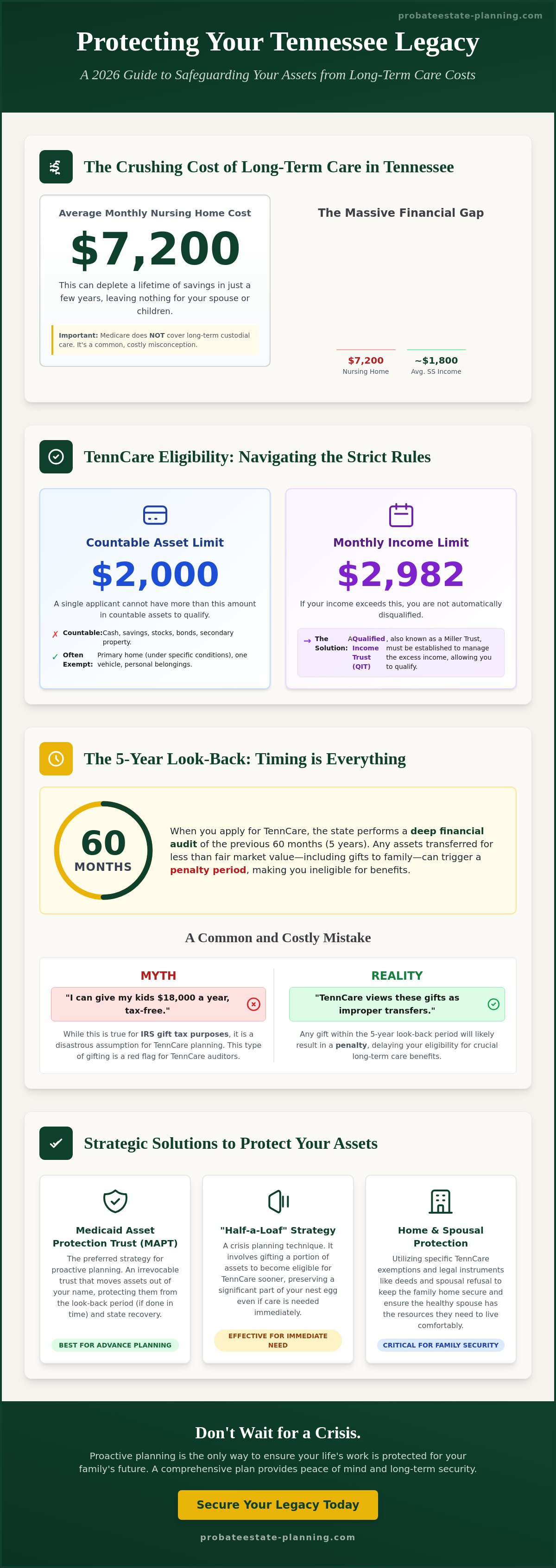

The cost of staying in a skilled nursing facility in Tennessee has reached a point where it can consume a lifetime of savings in a matter of months. Many families assume that Medicare will step in to cover these expenses, but this is a dangerous misconception. Medicare generally only pays for short-term rehabilitation after a hospital stay; it doesn't cover the long-term custodial care required for most nursing home residents. Without a clear understanding of how to protect assets from nursing home in tennessee, families are often forced into a "spend down," which is a process where you must exhaust nearly all your resources until you are poor enough to qualify for state assistance. This is a trap for the unprepared that can leave a healthy spouse with nothing and eliminate any inheritance for the next generation.

To better understand the strategies available to safeguard your legacy, watch this helpful video:

Projected Costs of Care in Tennessee for 2026

As of May 2026, the average monthly cost for a private-pay nursing home in Tennessee is approximately $7,200. This figure varies significantly across the state. In metropolitan areas like Nashville and Memphis, you might see rates exceeding $8,500 per month, while facilities in Knoxville or more rural parts of East Tennessee may hover closer to the state average. Comparing these costs to the average Social Security or pension payment reveals a massive financial gap that can quickly lead to the total depletion of a nest egg. This disparity makes early planning essential for anyone who wants to preserve their home and savings for their loved ones.

TennCare Eligibility: The 2026 Income and Asset Thresholds

TennCare is Tennessee's Medicaid program, and its eligibility rules are strict. To qualify for long-term care benefits as a single applicant in 2026, you cannot have more than $2,000 in countable assets. This $2,000 limit is often misleading because many people don't realize which assets the state counts toward this total. While your primary residence may be exempt under specific conditions, your cash, stocks, and secondary properties are usually at risk.

Income is another hurdle. The income limit for a single applicant is currently $2,982 per month. If your monthly income exceeds this amount, you aren't necessarily disqualified, but you must establish a Qualified Income Trust (QIT) to redirect the excess funds. These rules were significantly tightened by the Deficit Reduction Act of 2005, which also codified the five-year look-back period. Navigating how to protect assets from nursing home in tennessee requires managing these specific thresholds with precision to avoid a denial of benefits or a lengthy penalty period. Proper stewardship of your family's future starts with recognizing which assets are countable and which can be legally protected through strategic planning.

The 5-Year Look-Back Rule: Why Timing is Your Biggest Asset

The look-back rule is a 60-month window where TennCare scrutinizes every financial move you've made. It's not just a surface-level review; it's a deep dive into your stewardship of your resources. If you're wondering how to protect assets from nursing home in tennessee, you must understand that the state looks for any instance where you gave away money or property to meet the $2,000 asset limit. According to the National Institute on Aging, long-term care needs can arise suddenly, making the timing of these transfers critical to your legal security.

A frequent and costly mistake involves the annual gift tax exclusion. Many people believe they can "gift" $15,000 or more to their children each year without consequence. While the IRS might allow this for tax purposes, TennCare does not. Any such gift made within five years of your application will likely trigger a penalty. This disconnect between tax law and Medicaid rules often catches families off guard, turning a well-intentioned gift into a significant legal hurdle that threatens your peace of mind.

What Qualifies as a "Transfer" in the Eyes of TennCare?

TennCare auditors define a "transfer of assets" as any instance where an applicant disposes of resources for less than their fair market value to qualify for benefits. This includes writing checks to grandchildren, transferring a deed to a family member for a nominal sum, or even making unusually large charitable donations. Even selling a car to a neighbor at a "friendship discount" can be flagged. If the state determines a transfer was improper, they won't simply ask for the money back; they'll withhold payment for your care for a specific period of time.

Calculating the Penalty Period

Tennessee uses a specific "divisor" to determine how long you must pay out-of-pocket before TennCare coverage begins. As of 2026, this divisor is approximately $7,200, which represents the average monthly cost of nursing home care in the state. To find your penalty, the state divides the total value of improper transfers by this number. This calculation is a cold, clinical process that ignores your personal circumstances or intent.

Consider a $50,000 gift made to a child four years ago. TennCare would divide $50,000 by $7,200, resulting in a penalty period of nearly seven months. The most dangerous aspect is that this penalty doesn't start when the gift is made; it starts when you are otherwise eligible for TennCare and have already run out of money. This creates a "gap" where the nursing home expects payment, but the state refuses to provide it. Proactive Asset Protection Planning is the most effective way to avoid these periods of ineligibility and ensure your care is funded without exhausting your family's inheritance.

Strategic Legal Instruments for Asset Protection

Once you understand the financial risks and the timing constraints of the look-back rule, the focus shifts toward the specific legal tools available to safeguard your legacy. Standard estate planning often relies on a Revocable Living Trust to avoid probate, but these documents generally offer no protection against nursing home costs because the assets remain under your direct control. To truly secure your life savings, you need a strategy that balances your need for a predictable future with the strict eligibility requirements of the state. Learning how to protect assets from nursing home in tennessee involves moving beyond basic wills toward specialized instruments designed for long-term care stewardship.

The Medicaid Asset Protection Trust (MAPT) Explained

The Irrevocable Trust, specifically a Medicaid Asset Protection Trust, is often considered the gold standard for Tennessee families. Unlike a revocable trust, a MAPT requires you to relinquish the power to revoke the trust or pull assets back into your own name. While this sounds daunting, it's a strategic move that removes those assets from your "countable" total in the eyes of TennCare. You cannot serve as your own trustee; instead, you might appoint an adult child or a trusted advisor to manage the trust's affairs. This structure provides a layer of protection that keeps your nest egg intact for your heirs while still allowing the trust to hold and maintain your primary residence.

Protecting the Family Home: Deeds and Titles

Your home is often your most significant asset, and Tennessee law offers specific protections for a "Community Spouse" who continues to live in the home while their partner receives care. In 2026, federal and state rules allow the healthy spouse to retain a portion of the couple's resources, known as the Community Spouse Resource Allowance, which can reach up to $162,660. However, the home remains vulnerable to "Estate Recovery" after both spouses have passed away. This is where TennCare seeks to file a claim against the estate to recoup the costs of care paid during the resident's life.

To prevent this, some families consider Life Estate Deeds. This legal arrangement allows you to retain a "life interest" in the property, meaning you have the right to live there for the rest of your life, while the "remainder interest" passes automatically to your beneficiaries upon your death. While simpler than a trust, life estates carry risks, such as the property becoming vulnerable to the creditors of your children. Another option for converting excess cash into a non-countable resource is a Medicaid-compliant annuity. This instrument turns a lump sum of money into a monthly income stream for the healthy spouse, effectively shielding that capital from being "spent down" on nursing home bills. Navigating how to protect assets from nursing home in tennessee requires choosing the right combination of these tools to fit your family's unique dynamics and long-term goals.

Crisis Planning: What to Do If You Need Care Now

Many families find themselves in a sudden medical emergency where a loved one requires immediate placement in a skilled nursing facility. While early planning is ideal, it's a common misconception that you've lost the chance to safeguard your legacy once a health crisis begins. Crisis planning is a mitigation strategy for immediate care that allows you to protect a substantial portion of your estate even when the 60-month clock is already ticking. Understanding how to protect assets from nursing home in tennessee during an emergency requires a methodical, step-by-step approach that prioritizes your family's financial security and emotional well-being.

The Tennessee "Half-a-Loaf" Strategy

This strategy is one of the most effective tools for families facing an immediate need for care. The process involves gifting approximately half of your countable assets to your heirs and using the remaining half to purchase a Medicaid-compliant private annuity. This annuity provides a monthly income stream that pays the nursing home bill during the penalty period triggered by the gift. Because the penalty and the annuity income are structured to end at the same time, you've effectively preserved half of the assets that would have otherwise been spent down to the $2,000 limit. This process requires precise legal and actuarial calculations to ensure the annuity meets TennCare's strict requirements, as any error could result in a denial of benefits.

Asset Transformation: Turning Countable into Exempt

Another powerful tactic involves transforming liquid cash into "exempt" resources that TennCare doesn't count toward your eligibility. This isn't about hiding money; it's about the strategic stewardship of your resources. You can use countable cash to pay off a mortgage on your primary residence or make necessary home repairs, such as installing a walk-in tub or a wheelchair ramp. These improvements increase the value of an exempt asset while reducing your countable cash. Other effective spend-down tools include:

- Irrevocable Burial Contracts: In Tennessee, you can prepay for funeral and burial expenses, which removes those funds from your countable asset total.

- Caregiver Agreements: You can legally pay a family member for providing care, provided there is a formal, written contract in place and the pay reflects fair market rates. This reduces your estate while keeping the money within the family.

- Purchasing Medical Equipment: Buying necessary items like hearing aids, specialized beds, or a modified vehicle can help meet the spend-down requirements while improving your quality of life.

Navigating the complexities of TennCare during a medical emergency shouldn't be a solo journey. If you are currently facing a placement or have been told you have "too much money" to qualify, reach out to our team for a Medicaid Crisis Planning consultation to explore your options. Even in the middle of a crisis, there are legal paths to ensure your spouse is protected and your legacy is preserved. Learning how to protect assets from nursing home in tennessee is possible at any stage, provided you have the right guide to steer you through the process.

Securing Your Legacy with The Probate & Estate Planning Co.

TennCare regulations are notoriously complex and unforgiving. A single error in a property deed or a misunderstanding of a trust provision can lead to a catastrophic denial of benefits, leaving your family to foot a $7,200 monthly bill entirely on their own. Attempting a DIY approach to asset protection often results in missed deadlines or improper transfers that trigger lengthy, expensive penalty periods. At The Probate & Estate Planning Co., our Tennessee attorneys specialize in the precise legal maneuvers required for effective stewardship of your estate. We understand that learning how to protect assets from nursing home in tennessee isn't just about filling out paperwork; it's about ensuring your spouse and children are never left in a state of financial chaos during a medical crisis.

Our team provides the wisdom and experience necessary to master how to protect assets from nursing home in tennessee, giving you the freedom to focus on your family rather than legal deadlines. We act as a steady guide through the dense thicket of Medicaid rules, providing a clear path that prioritizes your family's interpersonal relationships alongside their financial security.

Our Process for Tennessee Families

We begin every partnership with a comprehensive asset audit and risk assessment. This deep dive allows us to identify which of your resources are vulnerable and which are already protected under state law. From there, we move into the customized drafting of Asset Protection Planning instruments, such as Medicaid Asset Protection Trusts and protective deeds. These documents are tailored to your specific family dynamics, ensuring that your plan actually works when your health requires it most. We don't believe in one-size-fits-all solutions because every Tennessee family has a unique legacy to preserve. Our methodical approach ensures that every detail is accounted for, from the initial transfer of property to the final TennCare application.

A Partnership in Stewardship

Our firm operates as a Trusted Advisor, focusing on the long-term harmony of your family. We've helped families across the state preserve their family farms and long-time homes from being sold to pay for care. By acting as a steady guide, we alleviate the anxiety that often accompanies end-of-life planning. We prioritize your emotional well-being by providing a logical, step-by-step path toward eligibility and protection. This human-centric stance moves away from cold legalism and toward a protective partnership.

Don't wait for a medical emergency to force your hand and limit your options. Take the first step toward peace of mind and protect your assets today—schedule your consultation with our experienced legal team. Discover the confidence that comes from knowing your life's work is shielded and your family's future is secure. We are here to ensure that your legacy remains a source of harmony rather than a cause of stress.

Preserve Your Legacy and Find Peace of Mind Today

Protecting your life savings from the rising costs of long-term care requires a blend of early action and expert legal strategy. This guide has explored how the 60-month look-back rule serves as a strict timeline, why specialized trusts offer the gold standard for protection, and how crisis planning can still save a significant portion of your estate even during a medical emergency. Understanding how to protect assets from nursing home in tennessee is the first step toward ensuring your spouse is cared for and your children receive their intended inheritance.

At The Probate & Estate Planning Co., we offer specialized Medicaid Crisis Planning expertise and multi-state legal authority across Tennessee, North Carolina, South Carolina, and Maryland. Our empathetic, human-centric approach moves beyond simple document preparation to provide a partnership in stewardship. We're here to act as your steady guide through the complexities of TennCare, ensuring your family avoids chaos and finds lasting security.

Secure your family's future with a Tennessee asset protection plan. You've worked a lifetime to build your legacy; let us help you protect it with the meticulous attention to detail you deserve. You don't have to face these challenges alone.

Frequently Asked Questions

Can TennCare take my house if I go into a nursing home?

TennCare won't take your home the moment you enter a facility, but they may seek to recover care costs from your estate after you pass away. Your primary residence is generally an exempt asset while you or your spouse live there. However, without proactive planning, the state can file a claim against the property during probate. This makes it vital to understand how to protect assets from nursing home in tennessee to ensure your home stays in the family.

Is it too late to protect my assets if my spouse is already in a nursing home?

It's almost never too late to safeguard a significant portion of your estate through Medicaid Crisis Planning. Even if your spouse has already been admitted, legal strategies like the "half-a-loaf" gift and annuity approach can often preserve about half of your countable resources. These last-minute maneuvers require precise actuarial calculations to satisfy state auditors, but they offer a vital lifeline for families who didn't have the opportunity to plan years in advance.

What is the 2026 income limit for Medicaid in Tennessee?

For 2026, the gross monthly income limit for a single applicant seeking long-term care benefits in Tennessee is $2,982. This threshold is based on federal standards and applies to all sources of income, including Social Security and pensions. If your monthly income exceeds this amount, you aren't necessarily disqualified from receiving help. You'll simply need to establish a Qualified Income Trust to manage the excess funds and maintain your eligibility for TennCare coverage.

Does a Revocable Living Trust protect assets from nursing home costs?

A standard Revocable Living Trust does not shield your assets from nursing home costs because you still maintain direct control over the trust's resources. Since you can change or dissolve the trust at any time, TennCare considers these assets "countable" toward the $2,000 individual limit. To effectively shield your savings, you generally need an Irrevocable Trust. This specific legal instrument requires you to relinquish certain control in exchange for the long-term protection of your legacy.

How does the 5-year look-back rule work in Tennessee?

The look-back rule is a 60-month audit period where the state examines all financial transfers to ensure you haven't given away assets to qualify for benefits. Any gift or transfer made for less than fair market value within these five years can trigger a penalty. During this period, TennCare will refuse to pay for your care, leaving your family to cover the average $7,200 monthly nursing home cost in Tennessee entirely out of pocket.

What assets are exempt from the Medicaid spend-down in TN?

Certain resources are considered "non-countable" and don't need to be spent down to reach the $2,000 eligibility limit. These typically include your primary residence, one vehicle, household goods, and personal effects like jewelry or clothing. You can also keep irrevocable burial contracts and a small amount of life insurance. Strategic stewardship involves turning countable cash into these exempt categories to protect your family's financial future while still qualifying for the care you need.

Can I give my house to my children for $1 to protect it?

Selling your home to your children for $1 is considered an improper transfer and will result in a severe penalty period. TennCare auditors calculate the difference between the $1 sale price and the actual market value of the property. They use this total to determine exactly how many months you'll be ineligible for benefits. This is a common mistake for those researching how to protect assets from nursing home in tennessee without professional legal guidance.

What is a Qualified Income Trust (QIT) and do I need one?

A Qualified Income Trust, also known as a Miller Trust, is a legal tool used when your monthly income is higher than the $2,982 limit. By directing your excess income into this trust each month, you can satisfy TennCare's strict financial requirements. You absolutely need one if your income exceeds the state threshold, as failing to set it up correctly will lead to an automatic denial of your application, regardless of your medical need for care.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment