What if the greatest threat to your family home isn't the rising cost of long-term care, but a single mistake made during a stressful application process? You've worked decades to build a legacy, yet the fear of the 5-year look-back period often makes the prospect of seeking help feel like a gamble. It's common to feel overwhelmed by the strict distinction between income and asset limits, especially when your family's financial security is on the line. Learning how to apply for Medicaid in Maryland shouldn't feel like a walk through a legal minefield.

You deserve a clear path that prioritizes your peace of mind and protects your home. This guide provides a step-by-step framework for 2026 to help you secure the care you need without sacrificing everything you've earned. We'll break down the complex government requirements into manageable actions, ensuring you understand exactly how to qualify while preserving your family's stewardship. From documentation checklists to asset protection strategies, you'll gain the confidence to submit an application that actually works when your family needs it most.

Key Takeaways

- Understand the vital distinction between MAGI and Non-MAGI programs to ensure your application aligns with your specific long-term care needs and family goals.

- Master the step-by-step process of how to apply for medicaid in maryland by identifying which state portal serves as the correct gateway for your unique financial situation.

- Prepare with confidence using our comprehensive documentation checklist, ensuring you have the five years of financial records required to navigate the state's rigorous review process.

- Learn how the "Medically Needy" program can protect you from the "spend-down" trap, allowing you to qualify for assistance without sacrificing your family's hard-earned legacy.

- Recognize when your situation requires a "crisis" application and how strategic legal tools can be used to protect your assets and restore your family's peace of mind.

Understanding Maryland Medicaid: Long-Term Care vs. Health Insurance

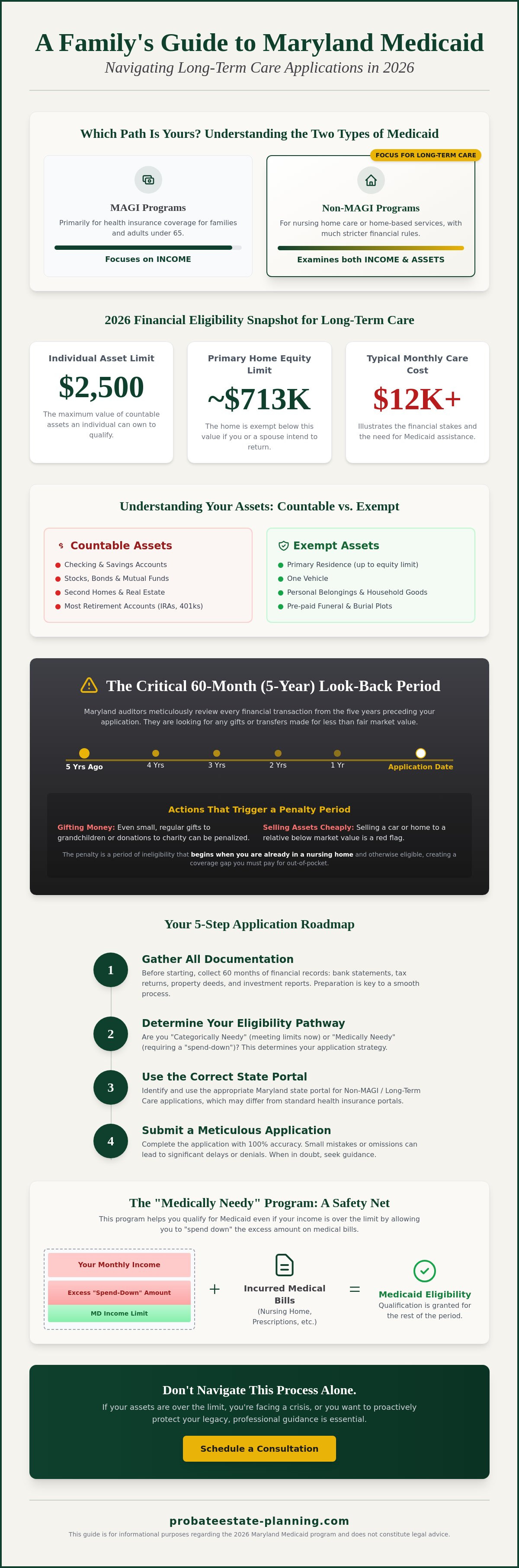

Transitioning into long-term care is one of the most stressful experiences a family can face. In Maryland, Medical Assistance (Medicaid) provides a vital safety net for those needing nursing home care or home-based services. Understanding the nuances of the Medicaid program is essential for protecting your family's legacy. It's not a single insurance plan but a complex system of programs designed for different needs. In 2026, the Maryland Department of Health and local Department of Social Services (DSS) offices continue to enforce strict distinctions between standard health coverage and long-term care benefits.

The process of learning how to apply for medicaid in maryland often reveals a divide between MAGI (Modified Adjusted Gross Income) and Non-MAGI programs. MAGI programs typically serve families and adults under 65, focusing almost entirely on income. However, long-term care falls under Non-MAGI rules. These standards are much stricter because the state is committing to pay for high-cost clinical care that can exceed $12,000 per month. This requires a thorough investigation into both your monthly income and your total accumulated wealth.

To better understand this concept, watch this helpful video:

Who is Eligible for Medicaid in Maryland?

Maryland offers two primary pathways to eligibility. The "Categorically Needy" pathway is for those who meet the strict income and asset limits immediately. In 2026, the individual asset limit for most long-term care programs remains at $2,500. The "Medically Needy" pathway, or "spend-down" program, allows people with higher incomes to qualify once they've incurred enough medical debt to lower their effective income below state thresholds. It's a vital safety valve for middle-class families facing catastrophic health costs.

Assets are divided into two categories under Maryland law:

- Countable Assets: These include checking and savings accounts, stocks, bonds, second homes, and most retirement accounts.

- Exempt Assets: Your primary residence is generally exempt if your equity is below the 2026 limit of approximately $713,000, provided you or a spouse intend to live there. One vehicle and personal belongings are also typically protected.

The Critical Importance of the 5-Year Look-Back Period

When you research how to apply for medicaid in maryland, you'll inevitably encounter the 60-month look-back rule. Maryland auditors meticulously review every financial transaction from the five years preceding your application. They're looking for any instance where you gave away money or sold property for less than its true value. Many families mistakenly believe that small gifts to grandchildren or donations to a church are exempt. They aren't. Even a series of $500 birthday checks can trigger a denial of benefits.

The penalty period is the duration of time that Maryland will refuse to pay for long-term care services based on the total value of assets gifted or transferred for less than fair market value during the look-back window. This penalty doesn't begin when the gift is made; it begins when you're otherwise eligible for Medicaid and have already moved into a facility. This timing can leave families in a precarious position with no way to pay the nursing home bill. Proper stewardship of your assets requires planning long before a crisis occurs.

Step-by-Step: How to Apply for Medicaid in Maryland

Success begins with a clear financial "snapshot." Before you log into any portal, gather your records from the last 60 months to account for the state's look-back period. This preparation prevents the administrative chaos that often leads to application denials. When you understand how to apply for medicaid in maryland, you realize the process is less about paperwork and more about proving your eligibility through meticulous stewardship of your records. You should have the following ready:

- Bank statements for all accounts held since 2021

- Proof of gross monthly income, such as Social Security award letters

- Life insurance policy details, including current cash surrender values

- Property deeds and recent Maryland tax assessments

Maryland utilizes two distinct digital platforms. Most applicants will interact with the Maryland Department of Human Services via the myMDTHINK portal or the Maryland Health Connection. Once you submit your materials, the state initiates a review period that typically lasts between 45 and 90 days. This window allows caseworkers to conduct both a clinical assessment of your health needs and a deep financial audit of your assets.

Method 1: Applying Online via Maryland Health Connection

This path is best for families seeking standard health coverage or community-based services. You'll start by creating a secure account on the Maryland Health Connection website. The system guides you through a series of logic-based questions about your household size and monthly income. To make the process manageable, use the "EnrollMHC" mobile app. It allows you to take photos of your tax returns or pay stubs and upload them directly to your case file. This digital trail ensures your documents aren't lost in the mail, providing much-needed peace of mind during a stressful transition.

Method 2: Applying for Long-Term Care (LTC) Medical Assistance

Nursing home Medicaid requires a more intensive, manual approach. Because the state is often paying for high-cost skilled nursing, the scrutiny is higher. These applications are frequently routed through the Bureau of Long Term Care in Baltimore. You aren't required to navigate this alone. You can request a face-to-face interview at your local Department of Social Services office to hand-deliver your application. This personal interaction helps clarify complex family dynamics that a computer algorithm might miss.

Protecting your legacy during this stage is vital; a well-structured estate planning strategy can ensure your application aligns with your long-term goals. If you prefer paper, you can mail a completed 9702 application form to your local office. Be aware that mailing physical documents often adds at least 14 days to the processing time compared to digital uploads. Regardless of the method, the goal is a plan that actually works when your family needs it most.

Checklist: Documentation Required for a Successful MD Application

Gathering the right paperwork is often the most stressful part of learning how to apply for medicaid in maryland. You're not just filling out a form; you're building a case for your future care and the protection of your legacy. Start with the basics of identity. You'll need original or certified copies of birth certificates and Social Security cards for both the applicant and their spouse. If you've served in the military, discharge papers are also necessary to verify potential veteran benefits.

Maryland follows a strict five-year look-back period. This means the state will scrutinize every financial transaction made 60 months prior to your application date. You'll need comprehensive records for all bank statements, 401k accounts, and IRAs. If you've transferred funds or made large gifts, be prepared to explain them with clear records. Income verification is equally vital. Gather current benefit letters for Social Security, private pensions, and VA benefits. The Maryland Department of Human Services uses these documents to determine if you meet the specific income thresholds for 2026. Don't forget your current health insurance information, including Medicare cards and any supplemental policy details.

Asset and Property Verification

Ownership of tangible assets requires clear documentation to ensure your application isn't delayed by technicalities. Collect deeds for any Maryland real estate and titles for all vehicles, including cars, boats, or motorcycles. If you hold life insurance policies, you must provide the current cash surrender value rather than just the death benefit amount. Professional appraisals are required for non-cash assets to establish their fair market value, which prevents the state from overvaluing your holdings and causing an unnecessary denial of benefits.

Shelter and Medical Expense Proof

If a spouse remains at home, mortgage statements and utility bills are critical for calculating the Community Spouse Resource Allowance. This protection ensures the healthy spouse isn't left in a state of financial hardship while their partner receives care. For those who exceed income limits, compile all unpaid medical bills from the last three months. These bills can often be used to meet spend-down requirements, which helps you qualify even if your income is slightly above the limit.

I recommend organizing every document in a dedicated Medicaid Audit Binder. Use dividers for each category: identity, financials, property, and medical expenses. This simple step brings order to a complex process and provides a sense of stewardship over your family's future. Having these records organized and ready ensures that when you're asked how to apply for medicaid in maryland, you can move forward with the quiet confidence that your plan is built on a solid foundation.

The "Spend-Down" Trap: Addressing Asset Protection Fears

Many families feel a sense of dread when they begin researching how to apply for medicaid in maryland. There's a persistent, frightening myth that you must be completely broke to receive help. This isn't the case. Maryland offers a "Medically Needy" path, which functions much like a deductible. You can use your mounting medical bills to offset your income until you meet the state's eligibility limit. While this provides a route to care, the emotional weight of watching your savings vanish is significant. Following the state's default "spend-down" is rarely the most efficient way to protect your family's future. It's a reactive approach that often leaves the surviving spouse vulnerable and the family's hard-earned legacy depleted.

The state's default process is designed for administrative ease, not for your family's financial health. When you simply spend until you hit the limit, you lose the ability to provide for your heirs or sustain a spouse remaining in the community. You have options to qualify without sacrificing every dollar you've worked for, provided you act with a clear strategy rather than in a moment of crisis.

Protecting the Family Home from Estate Recovery

The Maryland Medicaid Estate Recovery Program (MERP) is designed to recoup care costs from a recipient's estate after their death. For many, the home is their most significant asset and the centerpiece of their legacy. You should know that the state cannot take the home if a spouse, a child under 21, or a blind or disabled child still resides there. There's also a "Caregiver Child" exemption for children who lived in the home and provided care for at least two years before the parent entered a facility. Don't make the mistake of a "simple" deed transfer to your heirs. These transfers frequently trigger a 60-month look-back penalty, creating a period of ineligibility that can devastate a family's finances and leave you without care when you need it most.

The Community Spouse Resource Allowance (CSRA)

Maryland law protects the "well spouse" from becoming impoverished when their partner enters long-term care. This protection is known as the Community Spouse Resource Allowance. For 2026, these standards are adjusted to account for inflation, allowing the spouse at home to retain a significant portion of the couple's assets. Current projections for 2026 suggest a maximum resource allowance of approximately $154,140. Strategic reallocation of assets, such as purchasing a Medicaid-compliant annuity or making specific home improvements, can help you maximize this allowance. This ensures your spouse maintains their independence and dignity. If you want to secure your family's future and understand how to apply for medicaid in maryland without losing everything, it's vital to protect your legacy through strategic planningbefore the need for care becomes an emergency.

When to Consult a Maryland Medicaid Planning Attorney

Understanding how to apply for medicaid in maryland involves much more than simply completing paperwork. For many families, the application process is the final hurdle in a long journey of caregiving. While a "standard" application might work for someone with virtually no assets, most Marylanders possess a home, savings, or retirement accounts that they wish to preserve for their spouse or children. A mistake during the filing process can result in months of denied coverage, leaving the family to pay out-of-pocket for costs that often exceed $12,000 to $15,000 per month in skilled nursing facilities.

Our firm acts as a Steady Guide through the complexities of the Maryland Bureau of Long Term Care. We don't just help you fill out forms; we build a protective shield around your family legacy. By using Irrevocable Trusts, we can legally move assets out of your "countable" estate. This process ensures that your hard-earned resources are preserved for your loved ones rather than being entirely consumed by healthcare costs. We focus on the functional outcome, making sure your plan actually works when the crisis hits.

Proactive vs. Crisis Planning

The most effective way to protect your home and savings is to start at least 60 months before you anticipate needing care. This five-year look-back period is a strict rule used by the state to review every financial transfer you've made. Proactive planning allows us to utilize the full range of legal protections available under Maryland law. However, if a loved one is entering a facility tomorrow, don't lose hope. Through Medicaid Crisis Planning, we can often employ immediate strategies like Medicaid-compliant annuities or specific gifting patterns to save a significant portion of the estate, even at the last minute.

Your Next Steps for Peace of Mind

The first step toward security is scheduling a consultation focused specifically on the Maryland Medicaid landscape. When you meet with an elder law expert, it's helpful to bring the following items to ensure a productive session:

- Statements for all bank accounts and investment portfolios for the last several months.

- Copies of any existing estate planning documents, such as Wills or Powers of Attorney.

- Real estate deeds and recent property tax assessments.

- Documentation of all monthly income sources, including Social Security and pensions.

Knowing how to apply for medicaid in maryland is only half the battle; ensuring you qualify without losing everything is the real goal. We provide the clarity and authority needed to navigate this daunting landscape. A plan is the only way to ensure your legacy works when it's needed most, providing your family with harmony and protection during a difficult season of life.

Secure Your Family's Future Today

Navigating the complexities of Maryland's long-term care system requires more than just filling out forms. You've learned about the strict 60-month look-back period mandated by federal law and the specific documentation needed to avoid a denial. While understanding how to apply for medicaid in maryland is a vital first step, the real challenge lies in protecting the home and savings you've worked 30 years to build. Without a strategic plan, the state's asset limits can force families into a "spend-down" cycle that leaves little for a spouse or heirs.

At The Probate & Estate Planning Co., we specialize in Maryland-specific Medicaid regulations and crisis planning. We provide human-centric legal guidance to ensure your application is successful while safeguarding your legacy. Don't let the fear of tomorrow's costs disrupt your peace of mind today. We've helped families navigate these exact hurdles with a steady hand and a clear process.

You deserve the comfort of knowing your future is handled with care and precision.

Frequently Asked Questions

How long does it take to get approved for Medicaid in Maryland?

The Maryland Department of Health typically processes applications within 45 to 90 days. If you're applying based on a disability, the state has up to 90 days to issue a final determination. For standard medical assistance, you should receive a decision within 45 days. Completing your paperwork accurately ensures your family avoids unnecessary delays during this critical transition and secures the care you need.

Can I apply for Medicaid in Maryland if I still own my home?

You can apply for Medicaid while owning your home, provided it's your primary residence and your equity is below the 2026 state limit. In Maryland, a home is generally an exempt asset if the applicant, their spouse, or a dependent child lives there. However, the state may seek recovery from the estate after your passing. Planning ahead protects this legacy and ensures your home remains a source of stability for your loved ones.

What is the income limit for Maryland Medicaid in 2026?

The income limit for Maryland Medicaid depends on your specific category, but for most adults, it's 138 percent of the Federal Poverty Level. For long-term care, the 2026 monthly income limit follows the federal standard of $2,829 for an individual. Knowing how to apply for medicaid in maryland requires a clear understanding of these thresholds to ensure your eligibility remains intact. We help you navigate these numbers to find a secure path forward.

What assets are exempt from the Medicaid look-back period in Maryland?

Maryland exempts specific assets from the look-back period, including your primary residence, one vehicle, and personal belongings like furniture or jewelry. You can also set aside funds in an irrevocable burial contract or keep up to $2,500 in a designated burial fund. These exemptions provide a way to qualify for care without liquidating every family heirloom. Our focus on these rules helps you maintain dignity and financial security during a difficult time.

What happens if I gifted money to my family within the last 5 years?

Gifting money within the 60-month look-back period triggers a penalty period where you're ineligible for Medicaid benefits. The state calculates this delay by dividing the total value of gifts by the average monthly cost of nursing home care, which currently exceeds $10,000 in many Maryland regions. This penalty can create a gap in funding that leaves families vulnerable. Proper stewardship of your assets today prevents these painful complications later.

Can I apply for Medicaid on behalf of my elderly parent in Maryland?

You can apply on behalf of your parent if you're their legal guardian or hold a valid Power of Attorney. Maryland also allows you to act as an authorized representative by filing a specific state form during the application process. Taking this step allows you to safeguard your parent's health while managing the administrative burden for them. It's a vital part of protecting their legacy and ensuring they receive the high-quality care they deserve.

What is the difference between Medicare and Medicaid for long-term care?

Medicare only covers short-term rehabilitative care for up to 100 days, while Medicaid provides coverage for long-term custodial care in a nursing facility. Many families are surprised to learn that Medicare won't pay for extended stays. Understanding how to apply for medicaid in maryland is essential for those who need permanent support. This distinction is the foundation of a plan that works when your family needs it most, providing a predictable outcome for your future.

Do I need a lawyer to apply for Medicaid in Maryland?

You aren't legally required to hire a lawyer, but professional guidance is often necessary for families with complex assets or gifting histories. A single mistake on your application can lead to a denial or a lengthy penalty period that drains your savings. We provide the steady hand needed to navigate these regulations, turning a daunting process into a manageable one. Our goal is to offer you peace of mind through meticulous attention to every detail.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment