What if the family home you spent 30 years paying for wasn't actually yours to pass down? For many families in the Southeast, a single medical crisis or a $500,000 liability judgment can erase decades of hard work in a matter of months. You likely believe that your wealth should serve as a foundation for your children's future, not a fund for creditors or state recovery programs. It's a heavy burden to carry, which is why proactive asset protection planning is vital to ensure your property remains a legacy rather than a liability.

In this article, you'll learn how to build a legal fortress around your property and savings using state-specific strategies. We've designed this roadmap to move beyond the confusion of "hiding" money and focus on legitimate tools for North Carolina, South Carolina, Maryland, and Tennessee. We'll examine how to manage the 5 year Medicaid look-back period and use statutory protections to ensure your family's stewardship remains intact. We're providing a clear, actionable plan that complies with your local laws and provides the peace of mind your family deserves.

Key Takeaways

- Understand how to proactively shield your wealth from creditors and long-term care claims by utilizing proven legal structures rather than hiding assets.

- Discover the primary tools used to build a legal fortress, including how Irrevocable Trusts and LLCs can isolate your property from external risks.

- Learn why you must act before a legal crisis begins to avoid the pitfalls of fraudulent conveyance and ensure your protections remain valid.

- Explore state-specific asset protection planning strategies, such as homestead exemptions and Tenancy by the Entirety, tailored for residents of NC, SC, MD, and TN.

- See how a "Steady Guide" approach creates a functional plan that preserves your family's legacy and provides lasting peace of mind.

What is Asset Protection Planning and Why Does it Matter Now?

Asset protection planning is the proactive legal shielding of your hard-earned wealth from creditors, lawsuits, and long-term care claims. It isn't a strategy for tax evasion or hiding assets in secret accounts. Rather, it involves the strategic use of statutory exemptions and legal structures to ensure your family's security remains intact. To understand the foundational goals of these strategies, you can review this overview of What is Asset Protection? which outlines the legal framework for safeguarding property.

To better understand this concept, watch this helpful video:

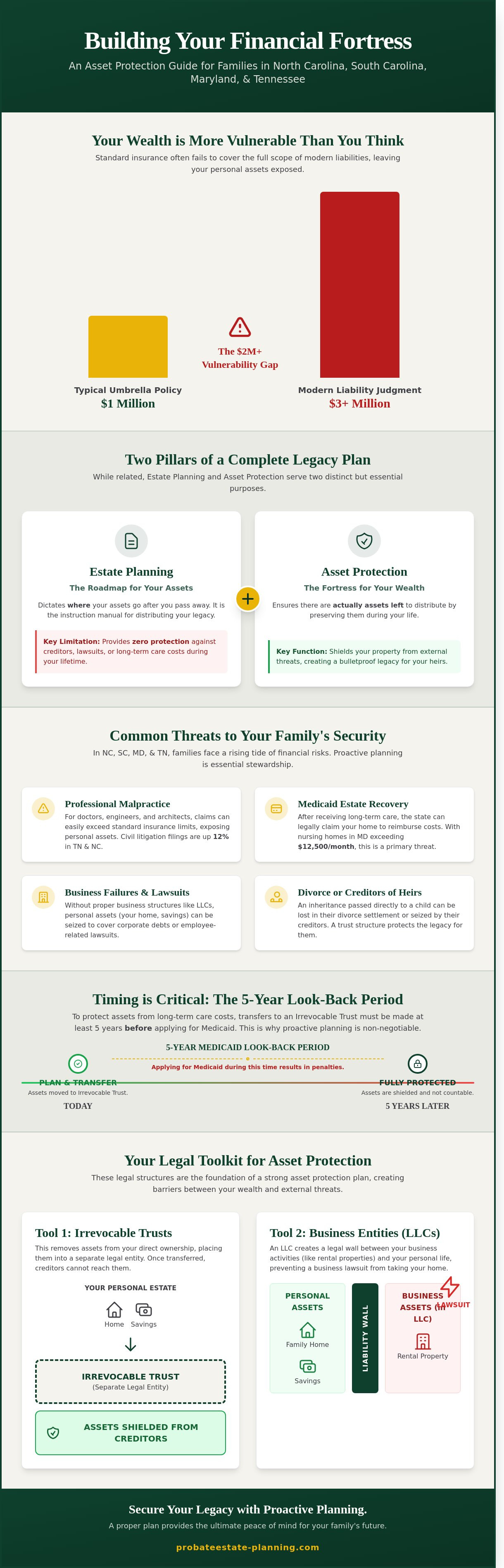

By 2026, the "vulnerability gap" has become a reality for many families in the Southeast and Mid-Atlantic. Standard insurance policies often fail to cover the full scope of modern liabilities. While an umbrella policy might provide $1 million in coverage, a single personal injury judgment in 2024 can frequently exceed $3 million. This planning isn't reserved for the "1%." If you own a home, a retirement account, or a small business, you have assets that are vulnerable to seizure without a proper shield.

The Difference Between Estate Planning and Asset Protection

Estate planning dictates where your assets go after you pass away; asset protection planningensures there are actually assets left to give. A simple Will provides zero protection against living creditors or the aggressive Medicaid spend-down requirements. While estate planning focuses on the transfer of wealth, asset protection focuses on the preservation of it. These two disciplines must work in tandem to create a bulletproof legacy. Without protective structures like irrevocable trusts or limited liability entities, your inheritance could vanish before it ever reaches your children's hands.

Common Risks to Your Wealth in NC, SC, MD, and TN

Residents in high-growth hubs face unique financial threats. In cities like Charlotte and Nashville, professional liability and frivolous lawsuits are on the rise. A 2023 study showed a 12% increase in civil litigation filings across Tennessee and North Carolina. Beyond the courtroom, the rising cost of long-term care poses a massive risk. In Maryland, the average monthly cost for a private nursing home room surpassed $12,500 in 2024. Without a plan, Medicaid estate recovery can legally claim your family home to reimburse the state for care costs. Common risks include:

- Professional Malpractice: Claims exceeding standard insurance limits for doctors, engineers, and architects.

- Medicaid Estate Recovery: State claims against your property after you receive long-term care.

- Business Failures: Personal liability for corporate debts or employee-related lawsuits.

- Divorce or Creditors: Claims made against heirs that can siphon away their inheritance.

Proactive planning isn't about paranoia; it's about stewardship. Taking these steps now provides the peace of mind that your family's future is not left to chance.

The Tools of the Trade: Building Your Legal Fortress

Effective asset protection planning isn't about hiding wealth; it's about organizing your life so that creditors and lawsuits can't dismantle your family's future. In states like North Carolina and Tennessee, the law provides specific mechanisms to shield what you've worked for. By using these tools proactively, you prevent the chaos that often follows a sudden liability claim or a health crisis. When you wait until a problem arises, it's often too late to build these defenses.

The Power of Irrevocable Trusts

An Irrevocable Trust is a fiduciary arrangement that removes assets from your taxable and reachable estate. When you move property into this type of trust, you relinquish legal ownership while often retaining a defined benefit. This creates a formidable barrier. If you're concerned about the cost of long-term care, timing is your most valuable asset. The 5-year Medicaid look-back period means that transfers must happen at least 60 months before you apply for benefits. If you wait until a crisis hits, these protections may not be available. This strategy ensures your home and savings remain a legacy for your children rather than being consumed by $10,000 monthly nursing home bills.

Using Business Entities for Personal Security

If you own rental properties in Maryland or South Carolina, holding them in your personal name is a significant risk. A single slip-and-fall accident could jeopardize your personal bank accounts and your primary residence. Using a Limited Liability Company (LLC) creates a legal partition between your business risks and your personal life. However, simply filing paperwork isn't enough. You must maintain proper stewardship to avoid "piercing the corporate veil," a legal theory where courts ignore the LLC if you mix personal and business funds. In 2024, proper corporate formalities remain the best defense against personal liability. Family Limited Partnerships (FLPs) offer another layer of protection, allowing you to shift the value of assets to the next generation while maintaining management control.

Beyond trusts and LLCs, you should understand the legal framework for asset protection provided by state statutes. Each state offers "exempt assets" that creditors generally cannot touch. For instance, North Carolina's homestead exemption and Tennessee's protections for life insurance proceeds provide a baseline of security. For high-level protection, some clients explore Domestic Asset Protection Trusts (DAPTs), which are now recognized in 20 U.S. states. These structures offer a sophisticated way to safeguard wealth while maintaining some level of access. If you're unsure which tool fits your family's needs, consulting with a dedicated strategist can provide the clarity you need to move forward with confidence.

Proactive vs. Reactive Planning: Avoiding the 'Fraudulent Transfer' Trap

The most vital rule of legal defense is simple; you can't buy fire insurance while your kitchen is already engulfed in flames. Effective asset protection planning requires a clear horizon. If you wait until a process server is at your door or a medical crisis is unfolding, your options shrink instantly. At that stage, moving assets often triggers "fraudulent conveyance" laws. These statutes allow a judge to void transfers if they believe you moved property specifically to hinder, delay, or defraud a known creditor. Your intent matters deeply to the court, and timing is the primary evidence they use to judge it.

Many families confuse proactive planning with "hiding assets," but they're fundamentally different. Hiding assets involves secrecy and often illegal non-disclosure. Proactive planning is a transparent, legal reorganization of your holdings during a "period of calm." Understanding What is Asset Protection Planning helps you realize that the goal isn't to disappear from the grid. Instead, it's about choosing the right legal structures, like irrevocable trusts or limited liability entities, before any trouble exists. This creates a defensible barrier that respects the law while prioritizing your family's long-term harmony.

Understanding the Look-Back Period

In North Carolina, South Carolina, Maryland, and Tennessee, the 60-month look-back period is a rigid reality for Medicaid eligibility. If you transfer your home or significant savings to your children within five years of applying for long-term care assistance, you'll likely face a penalty period of disqualification. This isn't just a delay; it's a financial gap that your family must fill out of pocket. We encourage stewardship over "panic-gifting." When you plan at least five years in advance, you preserve your legacy without leaving your children with a tax mess or a legal headache.

When is it 'Too Late' to Protect Assets?

It's generally too late to protect a specific asset once a claim has been filed or a specific liability has occurred. In our target states, the statute of limitations for creditors to challenge a transfer as "fraudulent" typically spans 4 years from the date of the transfer. If you're currently facing litigation, any new asset protection planning moves will be scrutinized under a microscope. The court has the power to claw back those assets, potentially leaving you in a worse position than if you'd done nothing. Starting your plan today, while things are stable, ensures your strategy remains legally defensible if a storm eventually arrives.

State-Specific Strategies for NC, SC, MD, and TN

Effective asset protection planning requires a granular understanding of state statutes. While federal laws offer a baseline, your physical location determines how much of your home equity or life insurance stays in your family's hands during a legal crisis. In North Carolina, the homestead exemption protects $35,000 of equity. This amount increases to $60,000 for individuals aged 65 or older if the property was previously owned as a joint tenancy with a deceased spouse. South Carolina offers a more robust shield, allowing individuals to exempt up to $67,100 in home equity as of 2024. Maryland sits lower at $27,900, while Tennessee provides a modest $5,000 for individuals, though this rises to $25,000 for those caring for minor children.

Tenancy by the Entirety: The 'Secret Weapon' for Couples

This form of ownership acts as a fortress for married couples in all four states. Tenancy by the Entirety treats a married couple as a single legal entity, making the property unreachable by individual creditors. If a husband faces a professional liability judgment in Towson, Maryland, the creditor cannot seize the family home if it's held in this manner. It's a powerful tool, but it's fragile. If the couple divorces or one spouse passes away, the protection vanishes instantly. We often recommend layering this with a trust to ensure the shield remains intact during life's transitions.

Homestead and Life Insurance Exemptions

Beyond the home, state laws vary wildly on personal assets. North Carolina General Statute § 58-58-115 provides a significant advantage by protecting life insurance proceeds from the creditors of a beneficiary. This ensures a widow's inheritance isn't drained by her own past debts. In Maryland, "tools of the trade" laws protect up to $5,000 in equipment necessary for your profession, which is a vital consideration for small business owners in the Baltimore area. These exemptions are not automatic; they must be correctly asserted during legal proceedings to be effective.

Retirement accounts like 401ks receive robust federal protection under ERISA, but IRAs rely on state-level exemptions. In North Carolina, your IRA is generally exempt from creditors, but Maryland law caps certain protections based on what's "reasonably necessary" for support. Local court tendencies also play a role. In Rock Hill, South Carolina, York County judges typically demand strict adherence to trust formalities; any slip in documentation can jeopardize your shield. Similarly, in Towson, Maryland, courts closely scrutinize the timing of asset transfers. If you move assets into a protective structure less than three years before a liability arises, the court may view it as a fraudulent conveyance. Proactive asset protection planningis the only way to stay ahead of these local variables. To begin securing your family's future, you can schedule a consultation for comprehensive asset protection planning with our team today.

How The Probate & Estate Planning Co. Secures Your Future

Effective asset protection planning isn't a one-time event; it's a commitment to your family's future. Our firm acts as a Steady Guide, moving beyond the simple drafting of documents to build functional plans that actually work during a crisis. We've seen how generic plans crumble under the weight of a legal challenge. Our approach ensures your assets remain shielded while you maintain the financial control and flexibility you need to live your life today.

Navigating the distinct statutes of North Carolina, South Carolina, Maryland, and Tennessee requires deep local expertise. For example, Tennessee's Investment Services Act offers specific trust protections that differ significantly from Maryland's domestic asset protection rules. We bridge these gaps for families with property or business interests across state lines, ensuring no asset is left vulnerable to regional legal nuances. We don't just provide a folder of papers; we provide a roadmap for your family's security.

A Personalized Partnership in Stewardship

A 2022 legal industry analysis revealed that approximately 60 percent of online, "cookie-cutter" trusts fail because they aren't properly funded or updated. We treat your legacy with more care than a software algorithm can provide. Our team prioritizes family harmony by creating clear legal structures that prevent disputes before they start. We also integrate Medicaid planning into our asset protection planning strategy, protecting your home and savings from being exhausted by long-term care costs that often exceed $100,000 per year.

Your Protection Starts with a Single Conversation

Securing your legacy begins with a Peace of Mind audit. During this initial meeting at our Charlotte, Nashville, Rock Hill, or Towson offices, we'll review your current holdings and identify potential risks. You should bring a basic summary of your assets, any existing estate documents, and a list of your primary beneficiaries. We typically move from the initial consultation to a fully implemented protection plan within 14 to 21 days.

- Charlotte, NC: Protecting business owners and growing families.

- Nashville, TN: Specialized trusts for high-net-worth individuals.

- Rock Hill, SC: Localized planning for cross-border families.

- Towson, MD: Comprehensive probate avoidance and asset defense.

Don't leave your family's stability to chance. Contact us today to schedule your consultation and take the first step toward a secure, predictable future. Your legacy deserves the protection that only a dedicated partner in stewardship can provide. We're ready to help you build a plan that stands the test of time.

Take the Next Step Toward Lasting Security

Protecting what you've built isn't just about filing paperwork; it's about ensuring your family avoids the chaos of legal uncertainty. Effective asset protection planning requires a proactive approach to navigate the unique statutes found in North Carolina, South Carolina, Maryland, and Tennessee. By establishing your legal fortress today, you avoid the complications of fraudulent transfer claims and the stress of reactive decision-making. Our multi-state practice provides the specialized expertise needed for Medicaid Crisis Planning, ensuring your legacy remains intact even during unexpected health transitions. We're committed to delivering plans that work when your loved ones need them most, providing a clear path through complex regulations across these 4 specific jurisdictions. You don't have to carry the weight of these decisions alone. Our team serves as your steady guide, offering the professional authority and empathetic support your family deserves. Let's work together to transform your concerns into a predictable, secure future for those you care about most.

Schedule your Asset Protection Consultation with a Steady Guide today

Your peace of mind is the greatest gift you can leave behind, and we're here to help you secure it.

Frequently Asked Questions

Is asset protection planning legal in North Carolina and Tennessee?

Yes, asset protection planning is entirely legal and ethical in North Carolina and Tennessee when you implement it before a legal claim arises. Tennessee specifically strengthened these rights through the Investment Services Act of 2007, which allows for the creation of self-settled asset protection trusts. In North Carolina, the Uniform Voidable Transactions Act governs how and when you can move assets. You must act proactively; if you transfer property after a lawsuit is filed, a judge can reverse the transaction as a fraudulent transfer.

Can I protect my house from a nursing home if I'm already 70 years old?

You can still protect your home at age 70, but you must act immediately to account for the 60-month Medicaid look-back period. According to the 2023 Genworth Cost of Care Survey, the median cost for a private room in a nursing home has risen to over $100,000 annually. By using an irrevocable trust or a life estate deed today, you start the clock on protection. Even if you need care before five years pass, partial protection strategies often save significant equity for your family.

Does a Revocable Living Trust protect my assets from a lawsuit?

No, a Revocable Living Trust doesn't provide any protection against lawsuits or creditors. Because you maintain the power to revoke the trust and control the assets, the law treats those assets as your personal property. For genuine asset protection planning, you need an irrevocable structure where you relinquish certain rights. This legal boundary is what prevents a judgment creditor from seizing your home or accounts. It transforms your estate from an easy target into a protected legacy for your children.

What is the '5-year look-back' rule for Medicaid in Maryland and South Carolina?

The 5-year look-back rule is a 60-month window where Medicaid officials in Maryland and South Carolina review all financial transfers for less than fair market value. If you gave a $40,000 gift to a relative in 2021 and apply for benefits in 2024, that gift triggers a penalty period. This penalty means Medicaid won't pay for your care for a specific number of months. Proper planning ensures you navigate these dates carefully so your care is covered without depleting your entire life savings.

Can creditors take my 401(k) or IRA in a lawsuit?

Your 401(k) is generally safe from all creditors due to the federal ERISA law of 1974. IRAs have different protections; they're shielded up to $1,512,350 in bankruptcy cases under the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005. However, if you face a lawsuit outside of bankruptcy, state laws in Maryland or South Carolina determine the level of safety. We often suggest additional layers of protection to ensure your retirement remains a reliable source of harmony and support for your surviving spouse.

How much does a comprehensive asset protection plan cost?

A comprehensive plan typically costs between $3,500 and $12,000 depending on the complexity of your family dynamics and the number of properties you own. While this is an investment, it's small compared to the $15,000 monthly cost of memory care in many metropolitan areas in 2024. A professional plan prevents the total loss of your estate to legal fees or medical bills. It provides a predictable outcome that keeps your family out of court and out of conflict during difficult transitions.

What happens if I transfer my house to my children to 'protect' it?

Transferring your house directly to your children is often a mistake that creates unnecessary risk. If your child gets divorced or files for bankruptcy, your home becomes an asset their creditors can seize immediately. You also lose the "step-up in basis" tax advantage, which can force your children to pay a 15% capital gains tax when they eventually sell the property. Using a specialized trust provides the protection you want without exposing your home to the personal financial troubles of your heirs.

Do I need a special lawyer for asset protection in Charlotte or Nashville?

You need an attorney who specializes in the specific statutes of North Carolina or Tennessee, as asset protection planning laws are not uniform across state lines. For instance, Tennessee's 2007 trust laws offer unique advantages that a general practitioner might overlook. A local guide understands how regional courts interpret trust documents and property titles. This expertise ensures your plan actually works when your family needs it most, providing a steady hand to navigate the complexities of local probate and tax codes.

Comments

There are no comments for this post. Be the first and Add your Comment below.

Leave a Comment